Tom Cochrane, Associate Portfolio Manager, Alternative Asset Management

As more investors seek alternative assets and greater flexibility, evergreen funds are gaining significant momentum across global private markets. Between 2017 and 2023, more than 400 evergreen funds launched globally, with capital now totalling approximately US $700 billion, or about 5% of the private markets. With annual growth nearing 30%, some forecasts suggest evergreen funds could account for 20% of the market within the next decade.

What Is an Evergreen Fund?

An evergreen fund is a type of investment vehicle designed without a fixed end date. Unlike traditional private equity or private credit funds, which typically operate with a defined lifecycle, evergreen funds allow capital to be continuously recycled. Returns generated from portfolio exits are reinvested into new opportunities, offering ongoing investor access and a long-term compounding effect.

These funds are positioned to play a growing role in the private markets, appealing to investors who prioritise liquidity, flexibility, and durability in their portfolios.

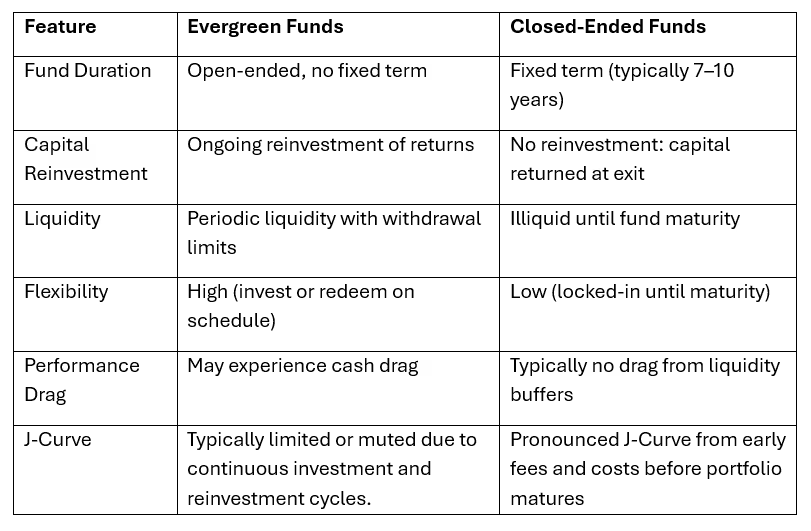

Evergreen vs Closed-Ended Funds: Key Differences

Notes:

- The J-Curve in closed-ended funds refers to the typical return profile where performance dips early (due to fees, setup costs, and uncalled capital) before rising as investments mature and generate returns. This effect is usually absent or less visible in evergreen structures because capital is invested continuously and returns are recycled

- Performance drag is a core trade-off for evergreen funds. The need to maintain cash or liquid assets to meet redemptions means less capital is working in high-return private market assets at any given time

The Liquidity Trade-Off in Evergreen Structures

Although the benefits of evergreen funds are substantial, the cost of the flexibility is cash drag. To maintain redemptions and subscriptions, evergreen structures must maintain a liquidity buffer consisting of cash or short-term bonds. For retail-focused vehicles, this reserve can be more substantial, with liquidity sleeves often representing up to 20% of total assets to support capped withdrawal requests. This liquidity requirement introduces an important downside: low-yield holdings with the potential to drag on fund performance, particularly in inflationary environments.

In contrast, closed-ended funds are typically able to deploy capital without the need to manage redemption flows, which can result in stronger long-term performance under the right conditions. These structures often outperform open ended equivalents across certain private market categories, though this advantage comes at the cost of significantly reduced liquidity and flexibility. Investors are locked in for the life of the fund, which is often 7-10 years or more. Closed-ended funds are also subject to a more pronounced J-Curve, where returns are initially negative due to fees or investment ramp up before improving later in the fund's life. Evergreen funds, by design, tend to avoid this J-Curve dynamic through ongoing reinvestment and continuous capital deployment, which smooths return profiles and supports compounding over time.

Why Transparency and Trust Are Critical

Investor trust is closely tied to understanding how liquidity works in evergreen or semi-liquid funds. As these funds enter the retail investment space, it's essential that fund managers disclose:

- Redemption limitations

- Liquidity buffer sizing

- Conditions for gating redemptions

According to Money Management (Private market providers risking adviser trust with misleading products | Money Management), lack of transparency can damage adviser confidence and client trust—two pillars that are crucial when introducing alternative fund structures to less experienced investors.

Final Thoughts: Are Evergreen Funds Right for You?

Evergreen funds represent an innovative entry point into private market investing, especially as more individuals and SMSF's seek alternatives to listed equities and term deposits. Their ability to offer recurring access, flexible entry/exit points, and ongoing reinvestment makes them attractive in modern portfolios.

However, investors must weigh these benefits against potential drawbacks, such as cash drag, redemption limits and performance dilution. In many cases, traditional closed-ended funds, though less flexible, offer more substantial long-term returns with reduced liquidity risk.

As evergreen funds continue to evolve, transparency and investor education will be essential. Understanding the structure, mechanics and trade-offs is crucial for making informed decisions that align with your investment goals.

FAQ: Evergreen Funds Explained

What is an evergreen fund in private equity?

An evergreen fund is an open-ended private market investment vehicle that reinvests proceeds from asset sales into new investments, with no set maturity date.

Are evergreen funds more flexible than closed-ended funds?

Yes. Evergreen funds typically offer periodic liquidity and allow investors to enter or exit at scheduled intervals, unlike closed-ended funds which lock in capital for fixed-terms.

What are the risks of evergreen funds?

The main risk is performance drag due to liquidity buffers. These funds also face redemption risk, which can lead to gating or limited withdrawals during periods of stress.

Do evergreen funds outperform traditional funds?

Not necessarily. While evergreen funds provide flexibility, traditional closed-ended funds often outperform over the long term due to full capital deployment and reduced cash drag.

At Prime Financial Group, we specialise in alternative asset strategies tailored to long-term wealth creation and succession planning. Whether you're considering evergreen structures, private equity, or property-backed alternatives, our team is here to help. Contact us today to explore strategic opportunities in private market investing.