2025 was defined by sharp market shifts, changing leadership across global markets and powerful capital flows — this is how our portfolios were positioned through the year.

The Year That Defied Conventional Wisdom

2025 will be remembered as a year when markets consistently surprised, challenged traditional ways of valuing investments and once again showed that liquidity and investor flows often matter more than valuations in the short term.

The Numbers Tell an Unexpected Story

While the general narrative suggested U.S. tech companies led the way, the actual performance data reveals a more nuanced picture:

- Gold: The standout performer, up more than 60% for the year

- Emerging Markets: Up almost 20% in Australian dollar terms

- Europe and Japan: Also up over 20% in Australian dollar terms

- Australian Equities: The laggard, up only modestly in single digits despite dividends

This divergence from the prevailing “Magnificent 7” and U.S.-centric market narrative highlights how more unloved parts of the market actually delivered superior risk-adjusted outcomes over the year.

A Year of Four Distinct Quarters

Q1: Looking Beyond the U.S

The year began with investors questioning whether U.S. markets and especially large technology stocks (Nvidia, Google) would continue to dominate. Money flowed into overseas equities instead, with investors betting on a more balanced global recovery.

Q2: Liberation Day Shock

The defining moment came in April with what became known as “Liberation Day” - when President Trump announced a dramatic escalation of tariffs. This pushed average U.S. tariffs to around 17%, effectively reversing three decades of trade liberalisation. Markets sold off sharply, with U.S. tech and small caps hit hardest.

Q3: Capital Flows Reverse Course

Here's where 2025 became truly surprising. Rather than triggering capital flight from the U.S., Liberation Day had the opposite effect. Companies and investors front-ran expected tariffs, accelerating capital flows into the United States. This unintended consequence, combined with strengthening AI narratives, fuelled a powerful rally that brought U.S. exceptionalism roaring back.

Q4: Doubts Emerge

By year's end, questions began surfacing about AI spending sustainability, return on investment, and whether China's more diversified approach (EVs, battery tech, energy-efficient AI) might prove more effective. The Fed's December rate cut, accompanied by cautious forward guidance and visible committee discord, added to the uncertainty.

The Great Divergence: U.S. vs Australia

A particularly striking feature of 2025 was the growing gap between U.S. and Australian bond markets. For most of the year, long-term interest rates in the U.S. and Australia moved closely together. But in the final quarter, Australian rates rose sharply as investors became more concerned about persistent inflation, weak productivity growth, and the Reserve Bank of Australia stepping back from expectations of near-term rate cuts.

Australian equities suffered accordingly, with extreme polarisation between defensive stocks like CBA and Wesfarmers, which remained elevated despite high valuations and well-known quality companies such as CSL, Ramsay Healthcare and Treasury Wine Estates, which fell out of favour.

The Liquidity Story: Flows Over Fundamentals

Perhaps the most important lesson from 2025 was that markets were driven less by the underlying health and value of companies, and more by the sheer flow of money moving in and out of markets.

U.S. Retail Mania: American individual investors poured an estimated $300–400 billion into exchange-traded funds that track the stock market, with significant flows into higher-risk products that magnify gains and losses. This wasn’t institutional money, making careful allocation decisions, it was individual investors buying what was already rising, pushing prices higher and encouraging even more buying.

Hedge Funds on the Back Foot: In a remarkable role reversal, professional investors found themselves trying to anticipate the behaviour of individual investors and follow the flow of money, rather than relying on traditional measures of company value and performance.

Australian Industry Funds: Similar dynamics played out in Australia, where superannuation flows into names like CBA pushed valuations to levels that would have been unthinkable in a fundamentally-driven market.

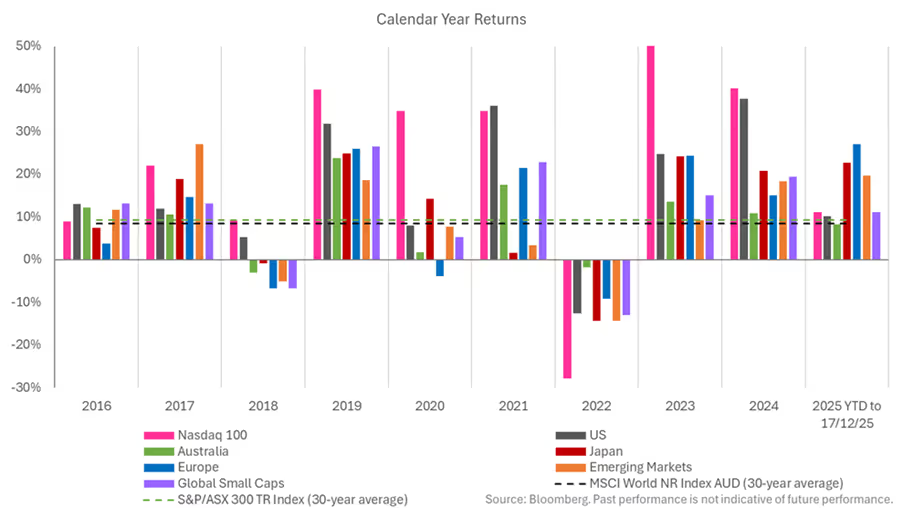

Historical Context: When Will the Music Stop? A 10-Year Perspective

The chart below tells a story that should give every investor pause - and paradoxically, every reason to remain humble about timing. What the chart below highlights is calendar year returns (in Australian dollar terms) for major equity markets across the globe.

What is striking is that the last 3-years has been characterised by double digit returns across most major equity markets. Historically and statistically having three consecutive years of double-digit returns is not that common and having most major equity markets achieve that feat also tends to be uncommon. Even looking at the last 10-years there tends to be a degree of dispersion between markets in any given year. Comparing the last 3-years to the last 30-year historical averages (as represented by the dotted lines) highlights how strong the last 3-years have been from a historical context. While the recent strength in markets should give us some pause for thought it doesn’t mean that markets can’t continue to perform but merely that we should be prepared for the possibility that going forward returns may not be as strong as they have been.

The extent of Nasdaq/Big US Tech leadership underscores the extraordinary nature of recent boom in markets:

- Nasdaq: Up over 200% in five years (despite the pull back in 2022), effectively delivering 20 years of expected returns in just five

- Global Equities: More than 10 years of expected returns compressed into five years

- Australian Equities: Roughly delivered what you'd expect over five years

These returns were boosted by the extraordinary government support that followed COVID. Unlike past crises, much of that money went directly into people’s and businesses’ bank accounts rather than staying trapped in the financial system. In the U.S. alone, around $10 trillion was created, with a large share still sitting in cash — money that could yet flow into markets and fuel further rallies.

What Made 2025 Different from 2024

While both years delivered strong returns, 2025 will be remembered for:

1. The Liberation Day Paradox: Policies meant to slow global trade were expected to damage markets but instead attracted more investment into the United States.

2. The Australian Underperformance: A stark reminder that not all markets participate equally in global rallies

3. The Retail Revolution: Individual investors, often using borrowed money, played a decisive role in pushing prices higher.

4. The Bond Market Divorce: U.S. and Australian long-term interest rates stopped moving together and began to diverge.

5. Emerging Markets Resilience: Solid performance despite trade tensions, suggesting markets increasingly differentiate by company quality rather than geography

The Valuation Question: Should We Worry?

With the extra return investors receive for taking risk near historic lows, and prices at elevated levels, the question on everyone’s mind is when does this end?

The honest answer is that we don't know. History shows these periods can persist far longer than seems rational. The late 1990s saw years of investors calling the top, only to watch markets climb another 20-30%.

What we should be prepared for:

- The probability that future returns may be lower than what investors have become used to.

- The chances of a market setback are higher than they have been in recent years.

- The timing of that setback remains unknown.

- Staying invested (but prudent) beats trying to time the exit.

Looking Ahead: Key Themes for 2026

As we close out 2025, several themes are emerging:

It's Too Early for Certainty: December 31st is just a date. With so many forces shaping markets at once, it makes sense to wait a few months before making bold predictions.

The Trump Administration's Policy Mix: With control of the Treasury, likely influence over the Fed by mid-2026, and more government spending on the horizon, the instinct will be to boost the economy rather than tighten the purse strings.

The Inflation Question: Any easing in inflation may be short-lived, setting the stage for renewed policy support and inflation pressures. This supports maintaining exposure to real assets, infrastructure, and companies with the ability to raise prices. As investors we should be for a range of outcomes and that means being prepared for potential shifts in inflationary outcomes either to the upside orthe downside.

Keeping Some Cash Available: When market timing is uncertain, having some money set aside allows investors to take advantage of opportunities when they arise.

Final Thoughts

2025 reinforced that in the tension between fundamentals and flows, flows often win in the short to medium term. Gold's 60%+ gain - a non-yielding, hard-to-value asset - serving as the year's top performer perfectly encapsulates this dynamic.

For professional investors, it was a humbling year that required staying invested despite stretched valuations, maintaining conviction in less-loved areas (emerging markets, global small caps, select Australian quality names), and not abandoning positions simply because markets kept moving higher.

As we head into 2026, the challenge is to stay invested while also keeping some flexibility for future opportunities. The risk of a market setback has increased, but trying to exit too early has proven costly, as markets often continued rising longer than expected.

The markets of 2025 reminded us once again that staying humble, diversified and focused on the long term remains the most reliable path when markets are running hot - even when those periods last longer than seems possible.

How have we managed these changes?

Throughout the year, we have implemented a series of measured portfolio adjustments in response to evolving market conditions, valuation dislocations, and shifting opportunity sets across asset classes. These changes were made systematically and deliberately, maintaining our focus on long term portfolio construction, diversification, and risk management principles. Rather than reacting to short term volatility, we sought to capture valuation opportunities as they emerged while ensuring portfolios remained appropriately positioned for their respective objectives.

The year presented distinct phases of market behaviour that required active but disciplined portfolio management. We maintained our commitment to valuation discipline as a core investment principle, which naturally guided capital allocation decisions during periods of both market stress and exuberance. This approach allowed us to rotate capital toward areas offering more attractive risk adjusted return prospects while reducing exposure to segments where valuations had become stretched or where structural risks had increased.

The information in this article contains general advice and is provided by Primestock Securities Ltd AFSL 239180. That advice has been prepared without taking your personal objectives, financial situation or needs into account. Before acting on this general advice, you should consider the appropriateness of it having regard to your personal objectives, financial situation and needs. You should obtain and read the Product Disclosure Statement (PDS) before making any decision to acquire any financial product referred to in this article. Please refer to the FSG (www.primefinancial.com.au/fsg) for contact information and information about remuneration and associations with product issuers. This information should not be relied upon as a substitute for professional advice, and we encourage you to seek specific advice from your professional adviser before making a decision on the matters discussed in this article. Information in this article is current at the date of this article, and we have no obligation to update or revise it as a result of any change in events, circumstances or conditions upon which it is based.