Market Data - April 2026

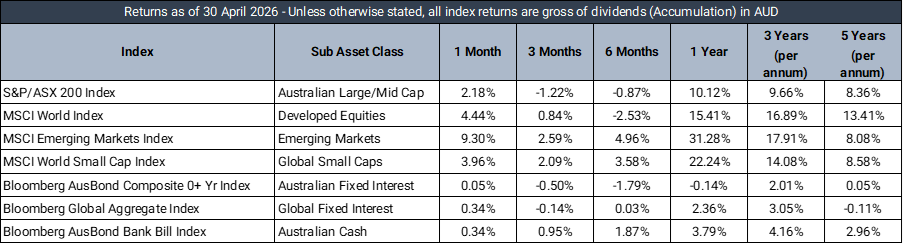

Market Returns - 1 Month to 30 April 2026 (in AUD)

Market Commentary

April 2026 was characterised by sharp intramonth swings as the U.S.–Iran standoff continued to dominate sentiment, keeping energy markets on edge. Despite this backdrop, global equities demonstrated remarkable resilience, with the S&P 500 reaching fresh all-time highs, underpinned by a strong earnings season in which more than 80% of companies beat revenue and earnings expectations.

International equity markets navigated a contradictory environment, with ceasefire optimism repeatedly giving way to renewed selling as diplomacy stalled. U.S. headline CPI rose to 3.3%, its highest since May 2024, driven by a sharp rise in energy costs. The Federal Reserve noted that inflation expectations remained anchored, though markets moved to price out rate cuts entirely for the remainder of the year. In Europe, German and French manufacturing slipped further into contraction as elevated energy bills weighed on output and consumer demand.

Domestically, performance was more nuanced than that of global peers. Energy producers outperformed while the banking sector came under pressure as institutions increased bad debt provisions. The unemployment rate held at 4.3%, though business confidence softened materially. The Australian dollar demonstrated notable strength, rallying toward 70.6 US cents, supported by a softer U.S. dollar and a temporary improvement in risk appetite. Hawkish rhetoric from the Reserve Bank of Australia persisted, as officials found little justification in the current data to shift toward a more accommodative stance.

Brent crude averaged $117 USD/barrel as the Strait of Hormuz closure tightened global supply, while bond yields rose broadly and Australian 10-year yields pushed toward 5%.

Looking ahead, the pace of diplomatic progress in the Strait of Hormuz and upcoming RBA meetings are the key variables to watch, with markets remaining sensitive to any data shifting the inflation or growth outlook.

Defensive Income

The Prime Defensive portfolio produced a +0.70% return over the month relative to a +0.34% target return. The portfolio has delivered a +4.62% return over the past 12 months, +0.84% above the target return.

April was a mixed month for fixed income markets, with credit spreads tightening across the risk spectrum while government bond yields moved modestly higher. Risk sentiment proved resilient, supported by stabilising macroeconomic data and a partial reversal of the prior month’s energy-driven inflation shock. In the US, economic data continued to reflect a resilient growth backdrop, with labour market conditions remaining firm and activity indicators generally outperforming expectations. This reinforced the market’s higher-for-longer view on Fed policy, contributing to a modest upward repricing in front-end Treasury yields. The UST 2-year yield closed the month 7bps higher at 3.87%, while the 10-year yield finished 5bps higher at 4.37%. Credit markets performed strongly despite the move higher in yields, with both investment grade and high yield spreads compressing as demand for carry remained robust and primary issuance was well absorbed. The 5-year CDX IG index tightened 9bps to +54bps, while CDX HY tightened 55bps to +330bps.

Domestically, rates also repriced higher as persistent inflation pressures and continued labour market strength reinforced expectations that the RBA would maintain a restrictive policy stance for longer. The ACGB 2y yield increased 11bps over the month to 4.77%, while the 10y closed 9bps higher at 5.06%. Australian credit markets broadly mirrored offshore moves, with spreads tightening across financials amid continued investor demand for elevated all-in yields. Our A$ Big Four Tier 2 5-year FRN Index tightened 9bps to +123bps, while the A$ Big Four Senior Unsecured Index tightened 5bps to +68bps.

Portfolio performance was strong over the month, with a large contribution from CIMHA (+2.00%). Duration exposure was once again a detractor, with offshore and domestic allocations – via Pimco Global Bond Fund and Pendal Government Bond Fund – returning -0.69% and -0.03%, respectively.

Australian Equities

The Australian equities portfolio returned 2.36% in April 2026, outperforming the ASX 200's +2.18% gain. The broader market recovered through the month as geopolitical tensions eased modestly and rate cut expectations firmed, supporting a rotation back into growth and interest rate-sensitive names that had been under pressure in prior months. Against this backdrop, the portfolio saw strong contributions from several growth and cyclical holdings.

Codan (+33.33%) was the standout performer, with Pilbara Minerals (+17.58%), Macquarie Group (+16.42%), Goodman Group (+15.82%) and Pro Medicus (+14.97%) also delivering strong gains as the ASX recovery broadened. Netwealth (+9.19%), REA Group (+8.59%), Medibank Private (+7.57%) and BHP (+6.61%) added further support, reflecting improved sentiment across growth, financials and resources.

These gains were significantly offset by Cochlear (-44.41%), which was the largest single drag on the portfolio following what appears to be a material company-specific event. CSL (-11.66%) and ResMed (-7.40%) extended weakness across healthcare, while Evolution Mining (-5.71%), Woodside Energy (-4.28%) and the major banks added modest headwinds. Overall, April's result was shaped less by broad market direction and more by concentrated healthcare weakness, particularly Cochlear, sitting against an otherwise broad-based recovery in the portfolio.

International Equities

The Prime International Growth Portfolio returned +5.3% in April 2026 versus the benchmark return of +4.44%, as global equity markets staged a powerful risk-on rally driven by a decisive rotation back into artificial intelligence and semiconductor-related stocks, with investors largely looking through the ongoing geopolitical tensions in the Middle East and surging oil prices to push the S&P 500 and Nasdaq to all-time highs.

The iShares S&P 500 AUD Hedged ETF (+11.1%) was the standout contributor for the month, reflecting the sharp recovery in US large-cap equities. The Munro Concentrated Global Growth Fund (+8.6%) and Munro Global Growth Small & Mid Cap Fund (+5.9%) also added meaningfully, with both managers' structural growth exposures well-suited to the AI-driven environment. On the other side, Trinetra Emerging Markets Growth (-2.8%) and the IFP Global Franchise Fund (-2.6%) detracted over the month, with the latter's quality-franchise style struggling against a backdrop that strongly favoured higher-beta, momentum-driven names.

Over the twelve months to the end of April, the portfolio returned +16.0%, a strong result underpinned by a broadening global equity rally. The iShares S&P 500 AUD Hedged ETF (+28.2%) was the largest absolute contributor over the period, while the Munro Concentrated Global Growth Fund (+23.3%), Plato Global Alpha (+27.7%), and Munro Global Growth Small & Mid Cap (+31.6%) all added significantly. The iShares MSCI Japan (+13.9%) and Pzena Global Focused Value (+13.8%) were also positive contributors, benefiting from Japan's pro-growth election outcome and continued corporate reform momentum. Partially offsetting these gains, Langdon Global Smaller Companies (-13.2%) and the IFP Global Franchise Fund (-4.3%) were the most significant detractors over the year, both facing headwinds from the AI-led mega-cap rotation that dominated much of the period. Aoris International (-7.3%) and Trinetra Emerging Markets Growth (-5.4%) also weighed on returns, with selective quality and emerging market managers finding the environment challenging relative to momentum-driven peers.

Balanced Multi-asset

The Prime Balanced Portfolio returned +2.0% in April 2026, reflecting the broad global equity rally driven by a decisive rotation back into AI and technology stocks, with investors largely looking through the ongoing Middle East tensions and surging oil prices. The portfolio's balanced and diversified nature meant that it participated selectively in the upside.

Global equities were the key driver for the month, with the iShares S&P 500 AUD Hedged ETF (+11.1%), Munro Concentrated Global Growth (+8.6%), and Munro Global Growth Small & Mid Cap (+5.9%) all contributing strongly. Within the alternatives sleeve, Resolution Capital Global Property Securities (+8.2%) added meaningfully, though Global X Physical Gold (-4.7%) gave back some of its recent gains as improved risk appetite reduced safe-haven demand. Australian equities were a modest drag, with Ophir High Conviction (-3.0%) continuing to struggle, while fixed income contributed only marginally as elevated RBA rate expectations kept government bond yields elevated and Pendal Government Bond (-0.03%) detracted.

Over the twelve months to the end of April, the portfolio returned +10.3%, with the fixed income sleeve a significant contributor, as the portfolio's preference for higher-yielding credit strategies over government bonds proved well-placed in a rising rate environment. MA Priority Income (+8.0%), Yarra Higher Income (+5.4%), and Realm High Income (+6.1%) all added value. Global equities contributed strongly through the iShares S&P 500 AUD Hedged ETF (+28.2%) and Munro Concentrated Global Growth (+23.3%), while Global X Physical Gold (+23.8%) anchored the alternatives allocation. Partially offsetting these gains, Trinetra Emerging Markets Growth Trust (-5.4%) and Langdon Global Smaller Companies (-13.2%) were the most significant detractors, with both managers facing persistent headwinds from the mega-cap and momentum-driven environment that dominated the period.

The information in this article contains general advice and is provided by Primestock Securities Ltd AFSL 239180. That advice has been prepared without taking your personal objectives, financial situation or needs into account. Before acting on this general advice, you should consider the appropriateness of it having regard to your personal objectives, financial situation and needs. You should obtain and read the Product Disclosure Statement (PDS) before making any decision to acquire any financial product referred to in this article. Please refer to the FSG (www.primefinancial.com.au/fsg) for contact information and information about remuneration and associations with product issuers. This information should not be relied upon as a substitute for professional advice, and we encourage you to seek specific advice from your professional adviser before making a decision on the matters discussed in this article. Information in this article is current at the date of this article, and we have no obligation to update or revise it as a result of any change in events, circumstances or conditions upon which it is based.