.avif)

Market Data - November 2025

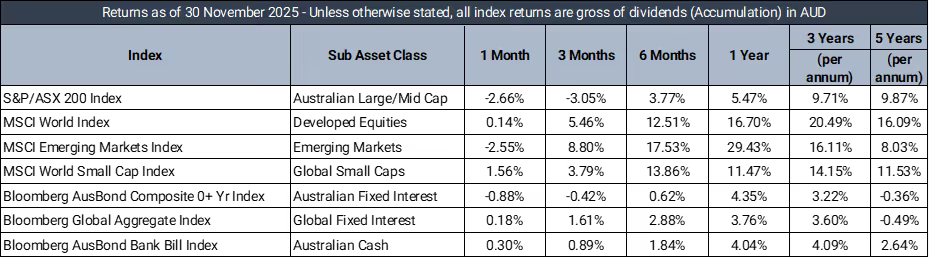

Market Returns - 1 Month to 30 November 2025 (in AUD)

Market Commentary

November 2025 was characterised by elevated volatility andrapidly shifting expectations, as investors navigated conflicting central bank signals and heightened sensitivity to macro headlines. A prolonged U.S. government shutdown added to uncertainty early in the month, but it was changes in interest rate expectations that ultimately set the tone for markets.

Global equity markets were mixed. U.S. equities continued to be driven by the AI-led rally, with mega-cap technology dominating index-level returns. Sentiment, however, became more fragile as concerns grew around valuations, increasing market concentration and the sustainability of investment flows across the AI ecosystem. Periodic sell-offs highlighted how quickly confidence can shift as investors reassessed whether elevated capital expenditure would translate into durable productivity gains. European markets softened amid weak manufacturing data, while Japan underperformed following a contraction in Q3 GDP. A temporary U.S.–China trade truce provided modest relief, though markets remained cautious about its longevity.

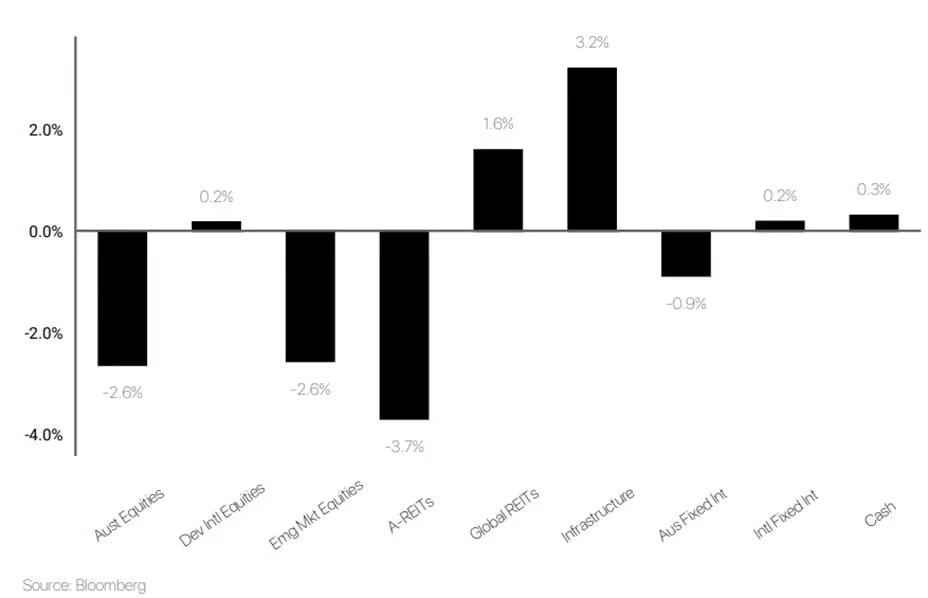

Domestically, Australian equities declined over the month as inflation surprised to the upside, reinforcing the Reserve Bank of Australia’s hawkish stance and pushing out expectations for rate cuts. Strong housing prices, robust credit growth and ongoing capacity constraints reduced confidence that inflation will return to target quickly, weighing on equity sentiment. In contrast, U.S. yields eased as markets increasingly priced further Federal Reserve cuts. In commodities, gold strengthened amid ongoing uncertainty, while oil prices fell on global oversupply concerns.

Looking ahead, markets remain focused on central bank policy divergence, valuation risks in global equities and whether AI-driven investment can deliver the productivity gains currently being priced in.

Defensive Income

The Prime Defensive portfolio was unchanged at a +0.006% return, relativeto the +0.30% benchmark return.

November was a mixed month for global fixed income, with U.S.Treasuries rallying early as softer data and lingering uncertainty aroundgovernment funding supported a bull-steepening move. The 2y yield fell sharplymid-month to lows near 3.48%, while the 10y briefly dipped below 4.00% beforeretracing as optimism around Fed rate cuts into 2026 tempered. Spreads in U.S.investment-grade credit held firm, while issuance remained heavy but largelyrefinancing-driven. The curve closed the month steeper, with 10y and 2y yieldsfinishing roughly -12bps and -15bps lower at 4.00% and 3.50%, respectively.

Domestically, the RBA held the cash rate at 3.60%, but persistent inflation (Q3 trimmed mean at 3.0%) and softer labour data pushed market expectations for easing into mid-2026. The ACGB curve was broadly stable, with the 10y yield finishing near 4.31% and the 2y up slightly at 3.60%, reflecting a modest bear-flattening bias early in the month before stabilizing. Local credit spreads continued to grind tighter, supported by strong demand for high-quality issuance, while floating-rate notes remain well bid amid elevated bill yields.

Australian Equities

The Australian Growth portfolio produced a –2.03% return over the month relative toa –2.66% return for the S&P/ASX 200 Accumulation Index.

November was a challenging month for Australian equities, with the S&P/ASX 200Accumulation Index falling –2.66% as global risk sentiment weakened and domestic macro data remained mixed. Financials led the decline, with major banks under pressure amid concerns over margins and slowing credit growth. Technology and consumer discretionary sectors also underperformed, reflecting global volatility and softer retail trends. In contrast, resources provided some offset, supported by strength in lithium and gold names, while select healthcare stocks posted gains.

Within the portfolio, broad market ETFs (A200 and IOZ) tracked the index lower, while individual holdings delivered mixed results. Exposures to CSL (+4.37%) and APA(+0.87%) contributed positively, alongside strong gains in EVN (+9.39%) and NEM(+11.93%) on commodity tailwinds. However, significant detractors included MQG(–8.37%), ALL (–7.13%), and technology names WTC (–10.26%) and XYZ (–10.89%).Overall, sector allocation and stock selection helped cushion the decline relative to the benchmark, with resource and healthcare exposures offsetting weakness in financials and technology.

International Equities

The Prime International Growth Portfolio returned -0.7% in November, in a month characterised by conflicting central bank signals andheightened sensitivity to macroeconomic headlines. While US equities continued to benefit from resilient earnings and leadership from mega-cap technology,broader global equity performance was mixed, with dispersion across regions andstyles influencing outcomes as small-caps and emerging markets lagged.

November performance reflected this divergence within theportfolio. Large-cap growth exposures were mixed, with Munro ConcentratedGlobal Growth (-4.2%) declining as high-multiple stocks consolidated following a strong run. In contrast, GQG Partners Global Equity (3.6%) was a notable contributor, benefiting from stock-specific strength and a more defensive regional mix. The Pzena Global Focused Value (0.9%) also added modestly, supported by improving sentiment toward financials and cyclically exposed businesses. Passive regional exposures were mixed, with the iShares S&P 500 Hedged ETF(-0.8%) modestly weaker, while the iShares Europe ETF (0.7%) added positively. These were offset by softness across several active strategies. Munro Global Growth Small & Mid Cap (-2.4%) detracted as small- and mid-caps lagged in a risk-averse environment, while Aoris International (-1.0%) also weighed modestly. Emerging market exposure through Trinetra (-0.8%) detracted as sentiment toward China and broader emerging markets softened, while Langdon Global Smaller Companies (-0.0%) was flat but continued to lag larger-cap peers.

Over the year to November, the portfolio delivered a strong absolute return, underpinned by sustained leadership from global growth equities. Plato Global Alpha (34.4%) and the iShares S&P 500 Hedged ETF(13.5%) were key contributors, supported by resilient US earnings and disciplined stock selection. Munro Concentrated Global Growth (21.2%) and Munro Global Growth Small & Mid Cap (17.7%) also added meaningfully. These gains were partially offset by weaker outcomes from GQG Partners Global Equity(-6.2%) and more subdued returns from global small-caps, with Langdon Global Smaller Companies (4.3%) reflecting ongoing dispersion across equity styles.

Balanced Multi-asset

The Prime Balanced Portfolio returned -0.3% in November, in a month characterised by conflicting central bank signals and heightened sensitivity to macroeconomic headlines. Equity markets were uneven, with ongoing strength in US mega-cap technology offset by weakness across Australianequities, small-caps and emerging markets, while bond markets reflected increasing policy divergence, shaping returns across the portfolio’s diversified structure.

November performance was supported by the portfolio’s defensive and diversifying exposures. Growth alternatives were a key source ofresilience, with Global X Physical Gold (4.3%) delivering strong gains as uncertainty remained elevated, alongside solid contributions from ClearBridgeRARE Infrastructure (4.0%) and Vanguard Global Infrastructure Index ETF (2.9%).Within equities, returns were mixed. Global value exposure through Pzena GlobalFocused Value (0.9%) provided modest support, while Munro Concentrated Global Growth (-4.2%) detracted as growth stocks consolidated following a strong run.Australian equities were a headwind, with Ophir High Conviction (-8.7%) the largest detractor amid weakness in domestic small-caps, alongside declines inthe iShares S&P/ASX 20 ETF (-4.4%). Emerging market exposure through Trinetra (-0.8%) also weighed modestly as sentiment softened.

Over the year to November, the portfolio delivered a solid absolute return, underpinned by diversification across growth, defensive and real assets. Global equities were a key contributor, with Munro Concentrated Global Growth (21.3%), iShares S&P 500 Hedged ETF (13.5%) and Vanguard All-World ex-US (25.0%) benefiting from resilient offshore earnings and equity market strength. Gold was a standout diversifier over the year, returning56.4%. Fixed income exposures also contributed steadily, supported by income carry and selective spread compression. These gains were partially moderated by weaker outcomes in selected active strategies and more subdued performance from global small-caps, with Langdon Global Smaller Companies (4.3%) reflecting ongoing dispersion across equity styles.

The information in this article contains general advice and is provided by Primestock Securities Ltd AFSL 239180. That advice has been prepared without taking your personal objectives, financial situation or needs into account. Before acting on this general advice, you should consider the appropriateness of it having regard to your personal objectives, financial situation and needs. You should obtain and read the Product Disclosure Statement (PDS) before making any decision to acquire any financial product referred to in this article. Please refer to the FSG (www.primefinancial.com.au/fsg) for contact information and information about remuneration and associations with product issuers. This information should not be relied upon as a substitute for professional advice, and we encourage you to seek specific advice from your professional adviser before making a decision on the matters discussed in this article. Information in this article is current at the date of this article, and we have no obligation to update or revise it as a result of any change in events, circumstances or conditions upon which it is based.