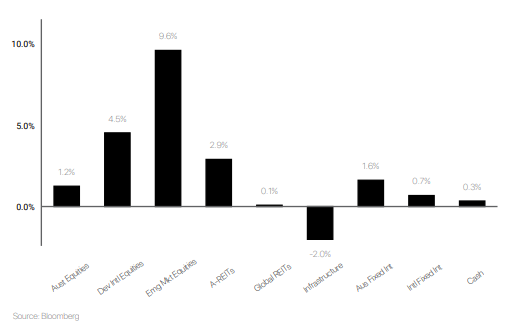

Market Data - May 2026

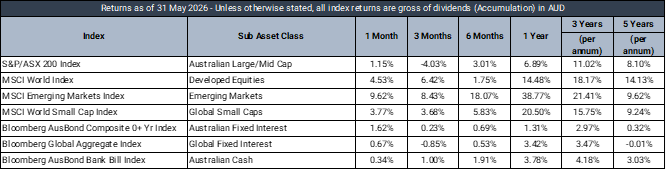

Market Returns - 1 Month to 31 May 2026 (in AUD)

Market Commentary

May 2026 was defined by ongoing escalations in Middle East tensions, as strikes on energy infrastructure in the UAE and the continued closure of the Strait of Hormuz introduced a significant risk premium across global markets. The resulting supply shock sent physical spot cargoes well above financial market benchmarks, setting the tone for a volatile month across asset classes.

International equity markets reflected the weight of rising energy costs and tightening financial conditions. Performance remained highly concentrated, with a narrow band of technology and energy names driving index returns, though May offered early signs of a potential "expectations ceiling", with some high-growth names finishing lower despite robust earnings. Consumer-facing sectors lagged as fuel costs and softening confidence weighed on sentiment. The transition to a new Federal Reserve Chair added to the uncertain backdrop, with long-end Treasury yields pushing to levels not seen in nearly two decades and rate-cut expectations fully unwound.

Domestically, the RBA raised the cash rate by 25 basis points to 4.35% in an 8-1 vote, its third consecutive hike this year. Later in the month, the unemployment rate rose unexpectedly to 4.5%, sharpening the RBA's trade-off between containing inflation and supporting a softening economy.

Brent crude averaged around US$106 per barrel over the month, bond yields rose broadly, and copper and iron ore reached multi-year highs.

Looking ahead, the persistence of energy supply disruptions and the path of central bank policy remain the key variables to watch. The widening tension between elevated energy costs and the capital demands of AI infrastructure adds a further layer of market sensitivity to any data that shifts the inflation or growth outlook.

Defensive Income

The Prime Defensive portfolio produced a +0.67% return (before platform administration fees) over the month relative to a +0.34% target return. The portfolio has delivered a +4.72% return over the past 12 months, +0.94% above the target return.

In the US, markets continued to grapple with the inflationary implications of the Middle East conflict, with surging energy prices driving both headline inflation concerns and a reassessment of the longer-end risk premium. Treasury yields were volatile throughout the month, with the UST 30-year yield reaching its highest level since 2007 before partially retracing. The UST 2- year yield closed the month 13bps higher at 4.00%, while the 10- year yield finished the month 7bps higher at 4.44%. Despite the move in rates, credit markets performed strongly, the 5-year CDX IG index tightened 4bps to +50bps, while CDX HY tightened 30bps to +300bps.

Domestically, fixed income markets outperformed offshore peers, with Australian government bond yields declining across the curve despite the RBA raising the cash rate by 25bps to 4.35% in May. The rally was concentrated late in the month following two data releases that softened the near-term policy outlook. April labour force data showed the unemployment rate rise 20bps to 4.5%, providing further evidence of labour market softening. This was followed by the April CPI, which printed at 4.2% year-onyear, below the 4.4% consensus, largely reflecting the government's temporary fuel excise reduction. Underlying inflation was less constructive, with trimmed mean CPI rising to 3.4% year-on-year, its highest level since late 2024. However, the headline undershoot was sufficient to moderate expectations for further policy tightening. As a result, the ACGB 2-year yield fell to its lowest level since mid-March, ending the month 25bps lower at 4.52%, while the 10-year yield declined 33bps to 4.83%. Australian credit spreads were largely stable and remained near cycle tights. Our A$ Big Four Tier 2 5-year FRN Index widened modestly by 2bps to +125bps, while the A$ Big Four Senior Unsecured Index was unchanged at +68bps.

Portfolio performance was strong over the month, with a large contribution from Pendal Government Bond Fund (+1.74%), as domestic duration outperformed.

Australian Equities

Australian equities portfolio returned +1.13%, in line with the ASX 200 as a broad rally in resources more than offset continued weakness in energy and healthcare. The RBA's third consecutive rate hike to 4.35% reinforced a hawkish backdrop, though improved commodity prices drove meaningful dispersion across the portfolio.

Materials and cyclicals were the standout contributors, led by Sandfire Resources (+20.36%), BHP (+15.99%) and Rio Tinto (+10.89%) on the back of strength in copper and iron ore prices. Wesfarmers (+9.42%), Pilbara Minerals (+7.31%) and Goodman Group (+7.07%) also contributed positively, reflecting selective rotation into quality and commodity-linked names.

On the negative side, Brambles (-26.78%) was the most significant detractor following earnings downgrades and operational setbacks in its US pallet network, while CSL (-22.32%) continued its de-rating amid persistent healthcare sector headwinds. REA Group (-12.28%), Netwealth (-9.30%) and Woodside (-8.61%) also weighed on returns, the latter pressured by easing oil prices as Middle East tensions showed tentative signs of stabilising. Overall, May reflected a tale of two markets — commodity-exposed names providing meaningful support while rate-sensitive and energy holdings remained a drag.

International Equities

The Prime International Growth Portfolio returned +4.3% in May 2026, as global equity markets pushed to record highs on the back of a robust earnings season, a pullback in oil prices as Middle East ceasefire talks progressed, and sustained investor appetite for artificial intelligence and semiconductor-related names.

The iShares MSCI Japan ETF (+7.4%) and iShares S&P 500 AUD Hedged ETF (+6.5%) were the strongest contributors over the month, reflecting broad gains across both markets. The Munro Concentrated Global Growth Fund (+7.2%) and Munro Global Growth Small & Mid Cap Fund (+5.4%) also performed well, with both strategies benefiting from an environment that firmly favoured growth over value. The other side of the ledger was led by Trinetra Emerging Market Growth (-3.0%), which faced a more difficult backdrop, while Langdon Global Smaller Companies (+0.5%) and the Maquarie IFP Global Franchise Fund (+0.2%) failed to keep pace with the broader rally.

Over the twelve months to end of May, the portfolio returned +14.4%, a result that reflects both the strength of its core growth holdings and the drag from a handful of more challenging positions. The iShares S&P 500 AUD Hedged ETF (+28.1%), Munro Global Growth Small & Mid Cap (+27.6%), Plato Global Alpha (+24.8%), and Munro Concentrated Global Growth (+21.5%) were all meaningful contributors over the period. Against this, Langdon Global Smaller Companies (-17.9%) was the standout detractor, weighed down by the persistent headwinds facing quality smaller companies in a concentrated market leader environment, while the Maquarie IFP Global Franchise Fund (-7.54%) and Trinetra Emerging Market Growth (-11.2%) also held back returns as quality-oriented and emerging market strategies struggled against the AI-driven momentum trade that dominated much of the year.

Balanced Multi-asset

The Prime Balanced Portfolio returned +1.7% in May 2026, a positive result that reflected the portfolio's more diversified positioning in a month that strongly rewarded equity risk. As global equity markets pushed to record highs on the back of a robust earnings season, easing oil prices, and continued AI-driven momentum, the portfolio's meaningful allocations to fixed income and alternatives tempered participation in the rally.

Within global equities, the iShares S&P 500 AUD Hedged ETF (+6.5%) and iShares MSCI Japan ETF (+7.5%) were the standout contributors, while Trinetra Emerging Market Growth (-3.1%) detracted and Langdon Global Smaller Companies (+0.5%) lagged. Alternatives were the weakest asset class for the month, with CBI Rare Infrastructure (-2.6%) and Resolution Capital Global Property Securities Fund (-0.4%) both declining, and gold (-1.5%) giving back some recent gains as risk appetite's rotated firmly toward equities.

Over the twelve months to end of May, the portfolio performed ahead of its benchmark, returning +8.9%, with fixed income and alternatives the primary drivers of that outperformance. The portfolio's active credit positioning delivered strongly over the year, with MA Priority Income (+7.3%), Yarra Higher Income (+5.6%), and Realm High Income (+6.1%) all well ahead of passive fixed income exposures. The Global X Gold ETF (+23.6%) and Fulcrum Diversified (+16.1%) added meaningfully within alternatives. On the other side, Australian equities were the key drag, with the Ophir High Conviction Fund (-7.5%) and Spheria Australian Small Companies (-0.3%) both struggling, while Langdon Global Smaller Companies (-17.9%) also weighed on the global equities sleeve as smaller quality companies globally faced a difficult environment.

The information in this article contains general advice and is provided by Primestock Securities Ltd AFSL 239180. That advice has been prepared without taking your personal objectives, financial situation or needs into account. Before acting on this general advice, you should consider the appropriateness of it having regard to your personal objectives, financial situation and needs. You should obtain and read the Product Disclosure Statement (PDS) before making any decision to acquire any financial product referred to in this article. Please refer to the FSG (www.primefinancial.com.au/fsg) for contact information and information about remuneration and associations with product issuers. This information should not be relied upon as a substitute for professional advice, and we encourage you to seek specific advice from your professional adviser before making a decision on the matters discussed in this article. Information in this article is current at the date of this article, and we have no obligation to update or revise it as a result of any change in events, circumstances or conditions upon which it is based.