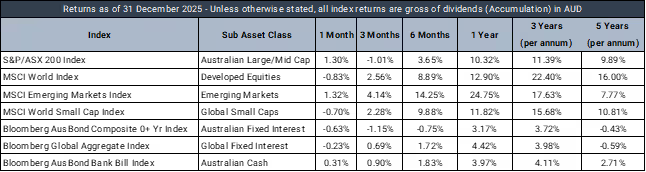

Market Data - December 2025

Market Returns - 1 Month to 31 December 2025(in AUD)

Market Commentary

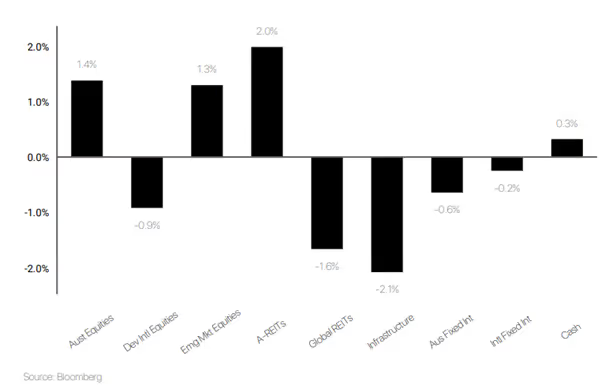

The fourth quarter challenged investors with contrasting central bank policies, stubborn Australian inflation, and sharp technology sector swings. International equities delivered solid returns with developedmarkets ex Australia returning 2.6% and emerging markets gaining 4.1%, whileAustralian equities declined 0.9% under pressure from rising yields. Europeanmarkets led with 5.8% returns as industrial production surprised positively, though U.S. equities faced December volatility when the Nasdaq fell 8% on AIvaluation concerns.

The quarter's defining theme was the stark policy split between major central banks. The RBA maintained its hawkish stance, with Governor Bullock's December comments revealing discussions of potential rate increases. This pushed the Australian 10-year yield above 4.6%, establishing a spread 0.5% higher than U.S. Treasuries which finished at 4.1%. Monthly CPI remained elevated at 3.8% by year end, with strong housing prices and record investment lending keeping the cash rate at 3.6%. Meanwhile, the Federal Reserve delivered a 25-basis point cut in November, the Reserve Bank of New Zealand appears to have completed its easing cycle, and the Bank of Japan moved toward tightening with two-year JGB yields reaching their highest levels since the Global Financial Crisis.

Regional divergence continued with U.S. China trade relations seeing October escalation followed by a temporary November truce. China struggled with contracting PMIs and retail sales growth falling to 1.3%, while New Zealand showed resilience with business confidence reaching an 11-year high. The quarter reinforced the value of global diversification as Australia's higher for longer rate environment contrasts with easing cycles elsewhere, creating both challenges and opportunities for portfolios navigating divergent monetary policy paths.

Defensive Income

The Prime Defensive portfolio produced a +0.29% return (beforeplatform administration fees) over the month relative to a +0.31% targetreturn. The portfolio has delivered a +5.51% return over the past 12 months,+1.54% above the target return.

In the US, the yield curve bear-steepened following the DecemberFOMC meeting. While the Fed delivered a widely anticipated 25bps rate cut andreiterated its focus on labour-market stability, policy expectations werealready well priced at the front end. As a result, the UST 2y finished themonth broadly unchanged, ending 1bp lower at 3.48%. By contrast, longer-datedyields moved higher as term premia rebuilt amid ongoing inflation uncertainty,with the UST 10y rising 15bps to 4.17%. Credit markets respondedconstructively. Investment-grade spreads tightened modestly, with the IG CDX 5yclosing 1bp tighter at +50bps, while high-yield spreads compressed moremeaningfully, narrowing 7bps to +317bps as risk appetite improved into yearend.

Domestically, Australian fixed income faced headwinds as yieldsrose across the curve. The 10y closed the month 22bps higher at 4.74%, whilethe 2y rose 25bps to 4.06%. Monthly CPI surprised to the upside, andlabour-market indicators remained robust, challenging the near-termdisinflation narrative. Market pricing continued to shift toward ahigher-for-longer cash-rate path, with an increasing probability of tighteningin 2026. Despite the rise in yields, credit spreads broadly tightened over themonth, with the A$ B4 T2 FRN 5y narrowing 3bps to +130bps, and A$ corporatehybrids FRN tightening 7bps to +171bps.

Portfolio performance closely mirrored the prior month, with MDIF(+0.73%) and MA PIF (+0.65%) again the top contributors, adding +9bps and +8bpsto overall returns, respectively.

While the drag from duration was less severe than last month, it continued to weigh on performance, with the Pendal Government Bond Fund (-0.73%) detracting 7bps.

Australian Equities

TheAustralian Growth portfolio produced a 0.64% return over the month relative toa 1.3% return for the S&P/ASX 200 Accumulation Index.

The market was largely supported by stronger commodity prices and improved sector sentiment. Materials led the market, boosted by gains in gold, silver, copper, and lithium, driving sector returns of 6.3–6.6% as miners benefitted from firmer metals prices and a softer US dollar. Financials also contributed meaningfully, rising 3.4–4.4%, helped by the Reserve Bank of Australia holding rates steady, which supported smaller financials and allowed major banks to recover from November’s weakness. Outside these areas, market performance was mixed. Real estate posted modest gains, but most other sectors finished the month weaker, reflecting ongoing caution around inflation and the prospect of elevated interest rates into 2026.

From a portfolio perspective, December's market dynamics translated into the top performers coming from the resources sector with Rio Tinto (+10.99%), BHP(+9.17%), Newmont (+7.70%), Evolution (+6.73%) and Pilbara (+4.20%). Followed by Financials, including Challenger (+5.97%), NAB (+5.51%), ANZ (+4.91%),Macquarie (+3.13%) and Westpac (+2.69%). These performers were largely offset by the healthcare and technology sector as Nanosonics (7.24%), CSL (-7.33%),ResMed (-8.57%) dragged down.

International Equities

The portfolio delivered a modest gain of 0.2% in December asheightened volatility challenged global equity markets, particularly technologystocks which experienced an 8.0% Nasdaq correction driven by AI valuationconcerns. Despite this turbulence, the S&P 500 hedged exposure (+1.2%)provided stability alongside strong performances from Langdon Global SmallerCompanies (+2.3%) and Pzena Global Focused Value (+2.1%). European marketscontinued their fourth quarter strength with the iShares Europe position returning1.8%, benefiting from positive industrial production data that surprised to theupside throughout the quarter.

December's performance was partially offset by weakness ingrowth oriented positions, with the Munro Global Growth Small and Mid Capholding (-2.9%) reflecting broader technology sector volatility and emergingmarkets exposure through Trinetra (-1.8%) facing headwinds from continuedweakness in Chinese economic data. The portfolio's diversified approach acrossstyles and regions helped navigate the challenging month, with value orientedstrategies providing ballast against growth stock volatility.

Over the year, the portfolio's 13.9% return was driven bystrategic positioning in currency hedged US equities and European marketsduring a period of stark central bank policy divergence. The S&P 500 AUDhedged allocation (+27.4%) proved instrumental, avoiding the currency headwindsthat impacted unhedged exposures while capturing strong US equity performance.This currency strategy alone contributed significantly to relative performance,particularly as the Australian dollar remained resilient against the backdropof the RBA's higher for longer stance. European exposure (+25.0%) benefitedfrom industrial production surprises, while the Munro Concentrated Global Growth Fund's (+16.5%) large tech exposure still proved beneficial over the whole year.

Balanced Multi-asset

The portfolio navigated December's volatile conditions withresilience, staying flat at 0.0% as rising Australian yields and propertysector weakness offset gains in selected global equity positions. Thisdefensive outcome during a month marked by regional divergence and elevatedAustralian inflation pressures reflected the portfolio's balanced positioningacross asset classes.

Over the twelve month period, the portfolio's 10.7% returnbenefited from strategic positioning in alternative assets and global equityexposure. The standout performer was Global X Physical Gold, surging 54.3% asinvestors sought safe haven assets amid inflation concerns and central bankpolicy uncertainty, transforming from a hedge to a core appreciation driverthroughout the year.

International equity holdings contributed solidly, withiShares S&P 500 AUD Hedged advancing 27.4% and Vanguard FTSE All World exUS gaining 23.2%. Active management delivered through Munro Concentrated GlobalGrowth's 16.5% return and a strategic regional exposure to Japan through theiShares MSCI Japan ETF (+16.4%), both captured value during periods of marketdispersion.

Fixed interest positioning strengthened returns,particularly through MA Priority Income's 8.2% contribution, which capitalizedon elevated yield opportunities during the year. However, the Australian equitysleeve faced headwinds, with the removed Vanguard Total Stock Market positiondetracting through its 10.2% decline before being exited from the portfolio.Property and infrastructure holdings also challenged performance during theyear, though CBI Rare Infrastructure partially offset broader sector weaknessthrough its 13.7% annual gain despite December's 3.6% decline reflecting thequarter's higher for longer rate environment impact on real assets.

The information in this article contains general advice and is provided by Primestock Securities Ltd AFSL 239180. That advice has been prepared without taking your personal objectives, financial situation or needs into account. Before acting on this general advice, you should consider the appropriateness of it having regard to your personal objectives, financial situation and needs. You should obtain and read the Product Disclosure Statement (PDS) before making any decision to acquire any financial product referred to in this article. Please refer to the FSG (www.primefinancial.com.au/fsg) for contact information and information about remuneration and associations with product issuers. This information should not be relied upon as a substitute for professional advice, and we encourage you to seek specific advice from your professional adviser before making a decision on the matters discussed in this article. Information in this article is current at the date of this article, and we have no obligation to update or revise it as a result of any change in events, circumstances or conditions upon which it is based.