One of the most critical SMSF administration tasks is getting the SMSF Annual Return (SAR) lodged on time. As recently reported, the ATO is hyper-focused on non-lodgement this year, and recently increased penalties for those who miss SAR deadlines.

If you're running an SMSF or advising someone who is, here's what you need to know about the risks and penalties of poor record keeping and late lodgment.

When is the SMSF Annual Return Due?

The SMSF Annual Return (SAR) must be lodged with the ATO annually, combining:

- Income tax reporting

- Regulatory compliance reporting

- Member contributions

- Auditor details and audit outcomes

Lodgment is required by 28 February if your fund is established and has a tax agent. Otherwise, October 31 is the deadline for newly registered funds or funds not using a tax agent.

Every SMSF must be independently audited before the SAR is lodged. If your audit is delayed due to poor record-keeping or inaction, this can delay the lodgment. The ATO still considers this part of the process the responsibility of the trustee(s), and can apply multiple fines if an auditor is not appointed in time, or if the audit is incomplete.

The ATO will accept audit delays as an excuse for late lodgment of SAR only in exceptional circumstances, which we cover further in this article.

The Consequences of Lodging a Late SAR

The ATO is both tax collector and compliance regulator, scrutinising whether the SMSF adheres to superannuation rules, not just tax rules.

If late, or non-compliant, the ATO can apply a set of penalties and conditions against the Fund, and individual trustees. These conditions and costs escalate the longer the breach remains.

Fund Compliance Status

As soon as the SAR lodgment is more than 2 weeks overdue, the ATO can change the Fund’s Super Fund Lookup status to 'regulation details removed'. This restricts the SMSF from receiving rollovers and employer contributions.

Amongst other issues, the inability to receive contributions can risk cashflow problems if the Fund relies on regular deposits to pay regular outgoing costs like insurance, administration fees or loan repayments.

One of the more serious consequences is that repeated non-compliance, including consistently late returns, may lead the ATO to classify the SMSF as ‘non-compliant’, resulting in:

- The Fund being taxed at 45% on its income instead of the concessional 15%

- Ineligibility to receive superannuation guarantee contributions

- Increased scrutiny or audits in future years

Further, if a Fund has a poor lodgment history, the ATO can remove your Fund from the lodgment program, which offers some concessional due dates and extended deadlines to compliant funds. This puts extra pressure on trustees and tax agents to comply with the standard due dates.

Administrative Penalties (ATO Fines)

Failure to Lodge (FTL) Fines

Late lodgment or ‘Failure to Lodge’ (FTL) the SAR triggers a fine, which increases in cost, depending on how many trustees are involved and how long the return remains outstanding.

FTL penalties are calculated in penalty units, which are applied every 28 days (or part thereof) after the lodgment deadline. In November 2024, the value of one penalty unit was increased to $330. FTL penalties max out at 5 penalty points, or 140 days overdue at a cost of $1,650. This penalty applies to the Fund, not individual trustees, but are not considered a deductable expense of the SMSF.

Administrative Penalties for Trustees

In addition to the FTL penalty, trustees may personally face administrative penalties for failure to lodge a SAR and poor record-keeping. For individual trustee structures, these penalties are imposed per trustee, or once for Funds with a corporate trustee.

Trustees are personally liable for administrative penalties and can’t be paid for by the Fund.

For example, an SMSF with two individual trustees fails to lodge the SAR on time, prepare financial statements and keep proper records will receive the following fines totalling $14,850:

- A Failure to Lodge fine, worth $1,650 against the Fund

- Administrative penalties of $3,300 per trustee

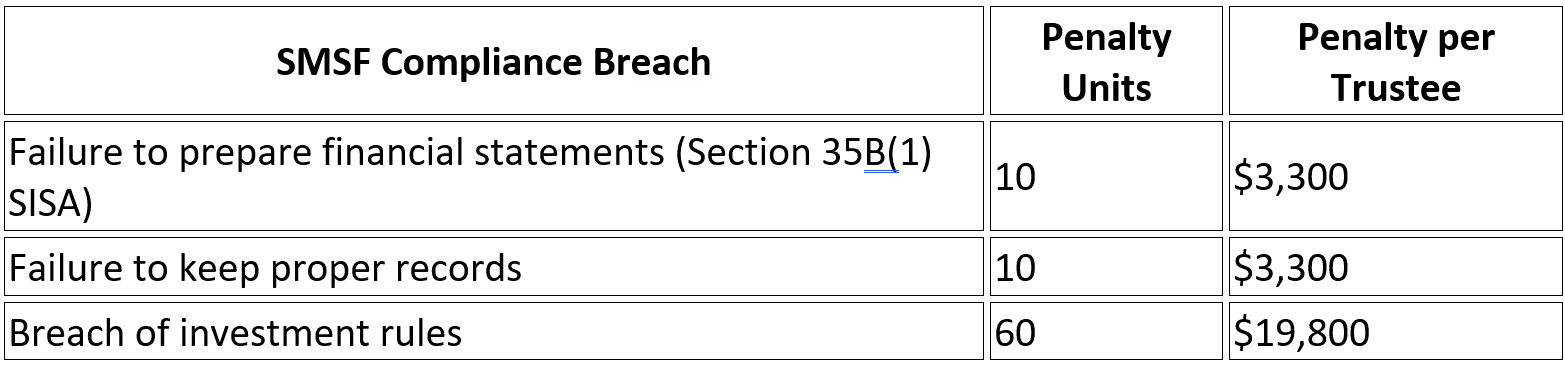

- $3,300 per trustee for failure to keep proper records

- Total fine per trustee ($6,600), combined for both trustees ($13,200), totalling $14,850.

Fines can quickly add up, and seemingly overnight, depending on how long the lodgement has passed the deadline.

Disqualification of Trustees

In severe or ongoing cases, the ATO has the power to disqualify trustees. This is publicly recorded and can have serious reputational and legal implications. Disqualified individuals cannot act as a trustee of any SMSF again.

Once the ATO notifies someone about their disqualification as a trustee or director of the corporate trustee, they must cease in their position as a trustee of the Fund. If someone is found to continue to act as a trustee or director of the corporate trustee once disqualified, further penalties may apply.

Can ATO Administration Penalties Be Remitted?

The ATO does sometimes reduce or waive administrative penalties if:

- There’s evidence of genuine hardship, illness, or extenuating circumstances

- The trustees acted in good faith and attempted to rectify issues quickly

- The fund has a generally strong compliance history

However, remission is not guaranteed and should never be relied upon as part of your strategy.

What If You Can’t Lodge the SAR on Time?

If you’re unable to meet your deadline due to valid reasons (e.g. illness, natural disaster, or unavoidable audit delays), you or your tax agent should contact the ATO as early as possible to request a lodgment deferral. The ATO is more likely to be lenient when you’re proactive and transparent.

How to Avoid Late Lodgment

It’s easier to maintain a compliant SMSF Fund if Trustees:

- Use a registered SMSF tax agent who can manage lodgment and communicate with the ATO on your behalf.

- Keep up-to-date records throughout the year. Don’t leave documentation until tax time.

- Engage your SMSF auditor early. Audits must be completed before the return can be lodged.

- Use SMSF software or an administrator to streamline reporting and record-keeping.

Lodging your SMSF Annual Return on time is not just good practice, but a legal requirement. The consequences of being late has significant implications, especially if it becomes a recurring issue. As a trustee, individuals are personally responsible for ensures their SMSF meets all its obligations.

When in doubt, speak with a qualified SMSF advisor or tax agent to avoid penalties and safeguard your retirement savings.