Market Data June 2023

Market Commentary

Over the quarter, hopes for a soft economic landing drove market optimism, with gains

seen across Europe, Japan, the US, and notably in the UK and ASX, but bond yields rise

posed potential threats to inflation control. China’s economic performance was slightly

weaker than expected, causing emerging markets to plateau.

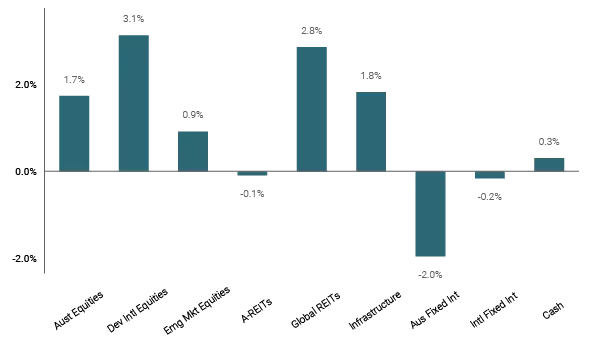

Looking back at the month, quarter, and concluded Australian financial year, there’s been

a general upward trend in markets with the most pronounced gains from Europe, US Tech

(Nasdaq), and Japan (25-30%), while the Australian market increased by 10%. Emerging

markets stayed flat due to China’s slow COVID recovery.

Western economic data has generally exceeded expectations, boosting US and

multinational earnings and consumer spending. Notably, US tech saw almost 20% gains,

outperforming the rest of the market which saw a modest 7% increase. Meanwhile,

challenges included rising Asian inventories, a modest recession in Germany, and

weakening in the US industrial sector.

Interest rates had minimal market impact this year. In the face of persistent inflation and

an increasingly hawkish Fed, the focus shifted to the slope of the US yield curve. The RBA

maintained lower short-term rates, causing a flatter yield curve. However, ongoing

inflationary pressures make the RBA mindful of potential future rate increases.

As the financial year closed, diversified Australian investors achieved 4-10% across the

risk profiles. Unlisted asset valuations, especially in industry funds, drew attention.

Struggling sectors like office space saw markdowns, suggesting a potential shift from

tailwinds to headwinds for industry funds. The Australian Retirement Trust reported a 15%

markdown in local office holdings, indicating an undervaluation of these assets or

overpricing in unlisted equivalents held by industry funds.

Market Returns – 1 Month to 30 June 2023 (in AUD)

Australian Equities

The ASX 200 increased 1.8% in June, with the Index up 9.7% for FY23. For the month of June Materials (+4.6%) was the best performing sector, while Healthcare (-6.4%) underperformed following the release of CSL FY24 earnings guidance, which was below market expectations. Overall, earnings expectations for the market continue to be revised lower ahead of the upcoming full year 2023 reporting period in August. We expect that company earnings will progressively be impacted by higher interest rates and ongoing cost pressures from wage and energy inflation.

During June there have been several key updates from companies in the portfolio, with Cleanaway Waste Management, CSL, and Ramsay Health Care providing earnings and/or operational announcements.

- Cleanaway – Reaffirmed FY23 earnings guidance of $300m EBIT and EBIT margin of 10.3% at its June Investor Day. CWY will provide 3-year EBIT CAGR targets at its FY23 result in August.

- CSL – Reaffirmed FY23 earnings to be towards the top end of guidance. However, FY24 guidance was below market expectations due to a more gradual recovery in gross margins and headwinds from FX and net interest costs.

- Ramsay – Announced it was exploring the possibility of a sale of its 50% holding in Ramsay Sime Darby (RMD Asia) after “receipt of significant inbound interest”. RHC also secured a new funding facility of A$1.5bn. The potential sale of RSD and refinancing would help to address concerns relating to RHC’s balance sheet.

At a portfolio level, BHP, Macquarie, and Woolworths were notable strong performing stocks. Whereas CSL, Northern Star and Spark NZ weighed negatively on performance.

Globally, central banks have been raising interest rates at the fastest rate since the 1990’s to tame persistent inflation. While the RBA held the cash rate steady at 4.10% in July, the RBA Board (along with US & European central banks) have reiterated their commitment that further tightening in monetary policy may be required.

In Australia, the effect of tightening by the RBA has begun to impact consumer spending but has been less potent in dampening house prices, which have risen consecutively over the past 4 months (CoreLogic). Indeed, a rapid recovery in migration levels combined with a tight labour market is providing an important ballast for the Australian economy.

For 2023 equity markets have been remarkably resilient, despite having to navigate the impact of higher interest rates (rising cost of capital), continued US/China/Russia geopolitical tensions, and consumer cost of living pressures, without a sustained drawdown in asset prices. The ASX 200 valuation metrics have been relatively stable based on a forward P/E of 14.5 times and a dividend yield of ~4.3%, both of which are trading around their 30-year average. The upcoming FY23 reporting period should provide an important indication of the health of company earnings and the prospects for the remainder of the year. The portfolio continues to hold industry leaders across the healthcare, industrial and resource sectors.

Defensive Assets

Again hindered by duration fears, June was a poor month for local bond markets with selling pressure continuing to push yields higher. Over the 2 months from the end of April 2023, the Australian 2-year and 5-year government yields have climbed 118 and 88 basis points, respectively. Interestingly, and unlike May, the weakness was specific to Australian bonds with the AusBond Composite (BACM0) Index falling -1.95% for the month, while the Bloomberg Global Aggregate (LEGATRUU) Index returned -0.01%.

Credit outperformed duration for the third straight month as the AusBond Credit FRN (BAFRN0) Index returned +0.41%. As with April and May, BAFRN0’s relative strength reflects a combination of tightening in credit spreads and the increasing benefits of carry with 3mBBSW finishing the month at 4.35%. Strength in credit markets was relayed by tightening of trading margins on BondAdviser’s AUD AT1 and AUD Tier 2 Indices over June. AT1 buying pressure was significant, seeing spreads on our All AT1 Index move from 305bps at 31 May to 270bps at 30 June, while Tier 2 trading margins came in 13bps over the month from 217bps. Total returns for the two indices were +1.56% and +0.31%, respectively.

The low exposure to local duration benefitted the Prime Australian Defensive Income Portfolio, which returned 23 basis points, though the portfolio did underperform the Bloomberg Bank Bill Index by 6bps.

With markets performing similarly to last month, the best and worst contributors in June were largely the same as in May. The Metrics Direct Income Fund added +9bps to the weighted result (+0.68% HPR), while the MA Priority Income Fund (+0.67% HPR) and MQGPF (+2.45% HPR) contributed +8 and +6 basis points, respectively. On an individual asset performance basis, MQGPF was the strongest in June, with its price rising from $101.36 to $103.84.

As was illustrated above by the plateau in global bond markets versus the drop locally, this was reflected by the PIMCO Global Bond Fund (+0.02% HPR) as opposed to the Yarra Australian Bond Fund (-2.10% HPR). This was the largest detractor from the Fund’s perfromance at -20bps.

Fund composition changed slightly over June with a 3% addition in the Yarra Higher Income Fund, accompanied by the 1% and 2% respective reductions in exposure to the Ardea Real Outcome Fund and the Realm High Income Fund.

International Equities

- The portfolio increased in value over June by 2.3%

- A number of large technology stocks, including Nvidia, Tesla, and Broadcom, drove

substantial market gains. The performance of these stocks underscored the significance

of the AI theme in markets over June. In the portfolio, this was reflected by the strong

performance of the Hyperion Global Growth Companies Fund, which returned 5.73%, as

well as the iShares S&P 500 ETF up +3.0% whereby these tech stocks alone carried the

whole S&P 500 to outperform the MSCI World Index. - The Aoris Internation and WCM Quality Global Growth Funds also outperformed the

MSCI World Index in June as their “quality-growth” factor was in favour for the month. - The Platinum International Fund was the only manager to finish June in the red. The fund

maintains a very defensive position, even for a value fund, and as a result has

implemented short positions on what it believes to be overvalued segments of the US

market. These shorts didn’t align with market movement for June and greatly detracted

as the US market continued its rally and stocks trading on high price-to-earnings ratios

further expanded. - Despite large equity falls coming out of China over the month, the Trinetra Emerging

Markets Growth Trust, which has roughly a 25% China exposure, managed to add +2.1%,

outperforming the MSCI Emerging Markets Index which was up only +0.9%.

Growth of $10,000 (Income reinvested) vs MSCI World Gross Total Return AUD Index

If you would like further details on Prime’s Separately Managed Accounts (SMA), please contact your friendly adviser or our client services team via e-mail on clientservices@primefinancial.com.au

Contact

Mark JohnsonT: (03) 8825 4738

Michelle BromleyT: (03) 8825 4751

Livio Caiolfa T: (03) 8825 4748

Nicole LewisT: (03) 8825 4734

Marcus AingerT: (02) 9134 6292

Gina McIntoshT: (07) 3557 2557

Dylan CresswellT: (03) 8825 4707

Brent QuinnT: (03) 8825 4705

Jarrod Rodda T: (03) 8825 4729

The information in this article contains general advice and is provided by Primestock Securities Ltd AFSL 239180. That advice has been prepared without taking your personal objectives, financial situation or needs into account. Before acting on this general advice, you should consider the appropriateness of it having regard to your personal objectives, financial situation and needs. You should obtain and read the Product Disclosure Statement (PDS) before making any decision to acquire any financial product referred to in this article. Please refer to the FSG (www.primefinancial.com.au/fsg) for contact information and information about remuneration and associations with product issuers. This information should not be relied upon as a substitute for professional advice, and we encourage you to seek specific advice from your professional adviser before making a decision on the matters discussed in this article. Information in this article is current at the date of this article, and we have no obligation to update or revise it as a result of any change in events, circumstances or conditions upon which it is based.