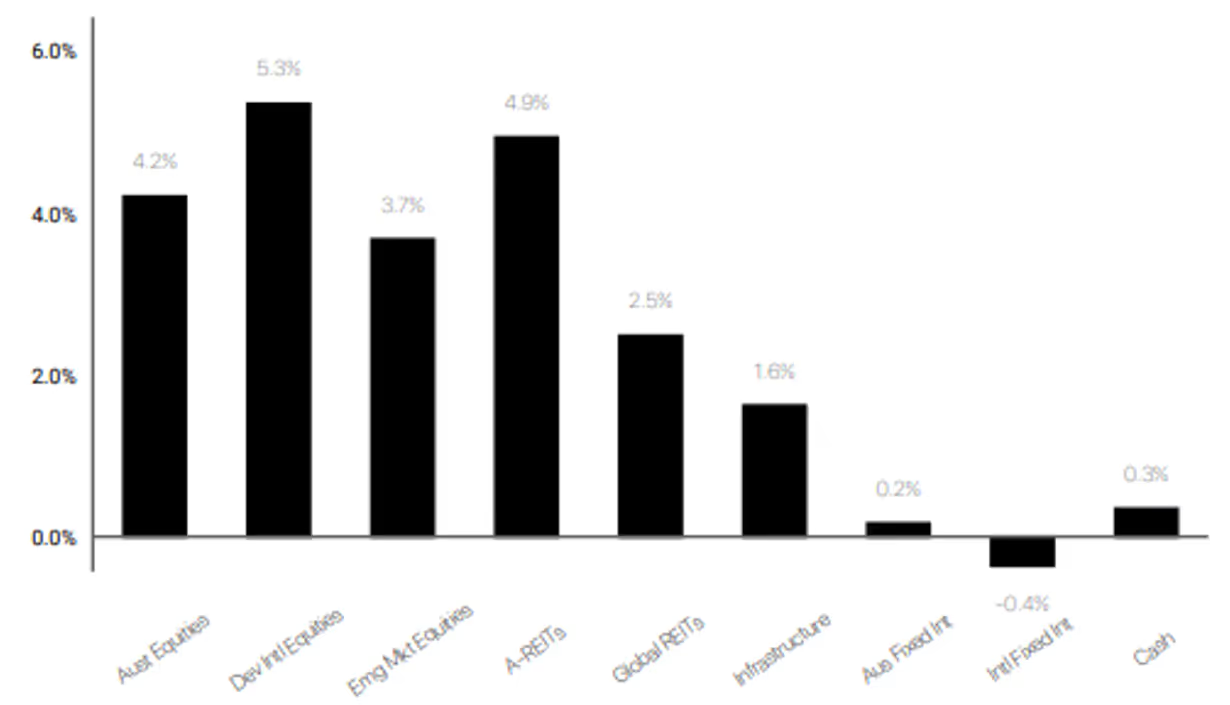

Market Data - May 2025

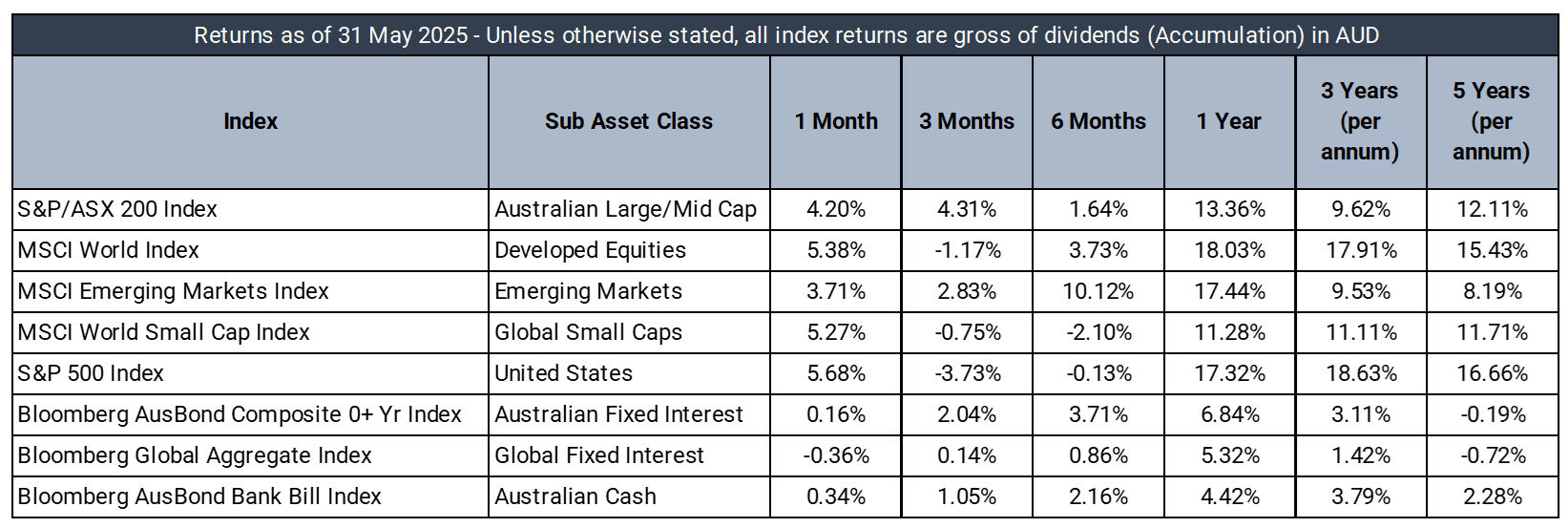

Market Returns - 1 Month to 31 May 2025 (in AUD)

Market Commentary

May 2025 saw markets whipsaw as investors grappled with shifting trade dynamics, mixed economic signals, and evolving central bank policies. The month began with a sharp rally, extending April's gains, as the U.S. and China reached a 90-day trade truce. However, sentiment remained fragile amid concerns over the fiscal position and debt sustainability of the U.S. following a Moody's credit rating downgrade and the passage of an expansive fiscal stimulus bill.

Global equities showed divergent performance, with U.S. stocks flirting with bull market territory on hopes a trade truce could pave the way for a more comprehensive agreement, while Europe and Japan posted more modest gains. Bond yields retreated mid-month, with U.S. 10-year Treasury yields falling 11 basis points in one week, on growth worries but resumed their climb as focus shifted to rising deficits. Escalating geopolitical tensions, weak Chinese industrial output and retails sales data, along with mixed corporate earnings results added to the uncertain backdrop.

In Australia, the RBA cut rates by 25bps to 3.85% during the month and signalled its willingness to ease further if required. Governor Michele Bullock emphasised potential risks to economic stability that could be underestimated by markets. The case for additional rate cuts was bolstered by lackluster GDP growth forecasts, with some banks projecting a sharp slowdown to 0.2% in the quarter, and the looming threat of global trade headwinds. Despite these challenges, the Australian dollar demonstrated resilience, reaching a year-to-date high even as the U.S. dollar strengthened broadly.

Looking ahead, markets remain highly sensitive to trade developments as U.S. negotiations with key partners continue. Investors are closely watching economic data and central bank signals for guidance on growth and policy paths. While worst-case trade outcomes were avoided in May, uncertainty and the impact of tariffs will likely keep markets on edge in the near term.

Defensive Income

May was a mixed month for global fixed income markets as volatility within markets continued. Spreads compressed from the widening in April, as high beta asset classes mostly recaptured March levels. The CDX HY 5y spread closed the month -57bps tighter at +351bps, as the prospect of trade resolution between China and the US became more viable. US government bonds sold off due to apprehensions regarding fiscal sustainability coupled with the Fed's concerns surrounding the prospect of continued high inflation. However, weak economic data reinforced bets that the Fed will lower interest rates twice before 2026, causing the 10y yield to fall from the intra-month high of 4.60% to close the month +24bps wider at 4.40%.

Domestically, the bond market saw a slight bear steepening in the yield curve. The ACGB 10y yield increased by +9bps to 4.25%, while our 2y was largely flat up +1bp to 3.28%. Domestic credit spreads compressed across the board as our Tier 2 5-year Major Bank FRN index fell -18bps to +171bps and the A$ True Corps BBB index fell -16bps to +138bps.

Prime delivered another solid month in May returning +0.53%. This stable performance contributed to an impressive 1y and 2y return of +6.92% and +6.75% p.a., outperforming the Bank Bill Index by +2.50% and +2.38%, respectively. Positively, this has been achieved with no negative months recorded in the last 2 years. This excellent performance has been achieved while maintaining consistently low exposure to interest risk (~1.5y duration) and high credit quality (A- portfolio average credit rating).

The top performers for the Portfolio were State Street Floating Rate Fund (+1.11%) and Metrics Direct Income Fund (+0.70%), contributing weighted returns of +14bps and +8bps, respectively. Pimco Global Bond Fund (-0.24%) was our largest detractor, returning -3bps as a function of off-shore duration underperformance.

During the month, we sold down the entirety of our remaining positions in MA1 and DN1. Some of the excess cash generated from this was quickly re-deployed into KKR Global Credit Opportunities Fund for c.2.5% of the portfolio. The transactions in May have also left us well positioned from both a liquidity and LIT exposure perspective to participate in the upcoming La Trobe Financial LIT which is due to commence trading in June.

Australian Equities

The Prime Australian Equities Portfolio delivered a 3.0% return in May as markets rallied on hopes of trade tension resolution, though the portfolio's concentrated positioning created mixed results. WiseTech Global (21.0%) emerged as the standout contributor, capitalising on in technology sector strength, while Ramsay Health Care (15.2%) benefited from defensive positioning amid economic uncertainty. Santos (9.7%) added significant value from the portfolio's overweight energy allocation, supported by stabilising oil markets, with Macquarie Group (12.8%) and Goodman Group (9.8%) further enhancing performance.

However, several key positions detracted materially. The substantial overweight in CSL (-1.6%) proved costly as the healthcare giant failed to participate in the broader rally, while Pilbara Minerals (-17.6%) suffered from ongoing lithium sector challenges. Treasury Wine Estates (-5.6%) and Nanosonics (-7.5%) highlighted the portfolio's vulnerability to consumer discretionary pressures amid persistent tariff-driven inflation concerns.

Over the twelve-month period, the portfolio's -1.4% return significantly lagged market gains, reflecting the challenging environment for active stock selection amid unprecedented trade policy volatility. The concentrated approach, while enabling outperformance during specific periods, proved vulnerable during extended uncertainty that characterised much of the year. Overweight positions in defensive names like CSL provided stability but missed risk-on rallies, while selective commodity exposure created headwinds when trade tensions weighed on resource demand. Most significantly, the portfolio's zero weighting in Commonwealth Bank, which delivered a humongous climb over the period, accounted for a large portion of the underperformance against the index as the major bank benefited from market flows, rising interest rate expectations and credit growth optimism.

International Equities

The Prime International Growth Portfolio navigated volatile market conditions in May, capturing gains despite significant trade tensions and fiscal concerns. Markets whipsawed on evolving U.S.-Europe trade negotiations, yet the portfolio benefited from strategic positioning during risk-on rallies that emerged following the U.S.-China trade truce.

Growth-oriented holdings drove May's performance, with Munro Concentrated Global Growth Fund (8.8%) leading contributions through its focused approach to quality companies. The fund capitalized on momentum-driven rallies and technology sector leadership. Nanuk New World Fund (8.7%) similarly benefited from the month's optimistic sentiment, while iShares S&P 500 AUD Hedged (6.6%) provided steady gains with valuable currency protection amid dollar volatility.

However, GQG Partners Global Equity (0.0%) struggled with flat performance, highlighting challenges for the more-active strategies in momentum-driven markets. The fund's disciplined valuation approach limited participation in risk-on rallies, though this positioning may prove beneficial during future market stress.

Over the twelve-month period, Munro's exceptional 26.4% return anchored performance, while Aoris International Fund (22.1%) and Japanese equities (19.6%) provided strong regional diversification. The removal of underperforming holdings like Platinum International Fund (-4.1%) and challenges with Pzena Global Focused Value (-3.6%) underscore the ongoing navigation of changing market leadership and style rotation in an uncertain global environment.

Contact

The information in this article contains general advice and is provided by Primestock Securities Ltd AFSL 239180. That advice has been prepared without taking your personal objectives, financial situation or needs into account. Before acting on this general advice, you should consider the appropriateness of it having regard to your personal objectives, financial situation and needs. You should obtain and read the Product Disclosure Statement (PDS) before making any decision to acquire any financial product referred to in this article. Please refer to the FSG (www.primefinancial.com.au/fsg) for contact information and information about remuneration and associations with product issuers. This information should not be relied upon as a substitute for professional advice, and we encourage you to seek specific advice from your professional adviser before making a decision on the matters discussed in this article. Information in this article is current at the date of this article, and we have no obligation to update or revise it as a result of any change in events, circumstances or conditions upon which it is based.

.avif)