Market Data - October 2025

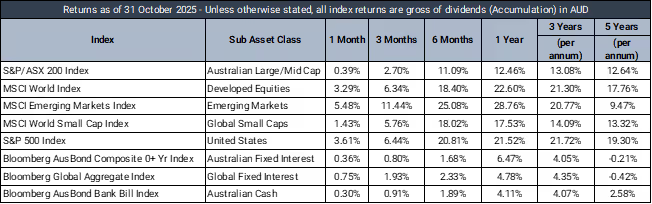

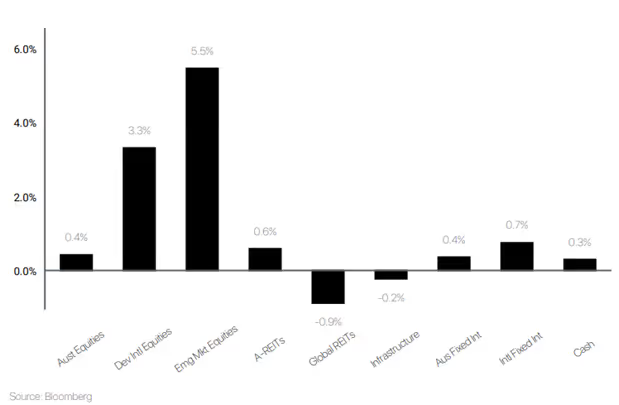

Market Returns - 1 Month to 31 October 2025 (in AUD)

Market Commentary

October 2025 was marked by a complex push and pull between robust equity markets and persistently elevated inflation, set against an increasingly unstable geopolitical backdrop. The month opened with investors digesting firmer-than-expected inflation prints, with U.S. PCE holding at 2.9% and Australia’s latest CPI at 3.0%, which kept the “higher for longer” narrative firmly in place and tempered expectations for aggressive global easing cycles.

Global equities were mixed but generally resilient. The Nasdaq outperformed, rising almost 4% as the AI theme continued to dominate sentiment, supported by AMD’s partnership with OpenAI and ongoing investment in AI infrastructure. That enthusiasm is now being tempered by uncertainty over productivity gains. Japan was another bright spot, with the Nikkei reaching record levels following Sanae Takaichi's election victory and the prospect of fiscal stimulus. Europe was weaker, particularly France, where political tensions and fiscal uncertainty kept investors cautious. Chinese equities improved late in the month as trade rhetoric softened.

Bond markets saw yields move higher across most regions, reflecting both inflation concerns and broader fiscal pressures. Australian 10-year yields rose before reversing sharply after the unemployment rate unexpectedly jumped to 4.5%, prompting markets to price in a potential December RBA cut. The U.S. dollar strengthened through the month, while the Australian dollar briefly slipped below US$0.65 amid risk aversion. Commodities were volatile. Gold surged to fresh highs above US$4,300 before giving back gains in a sharp mid-month correction, while oil rose on Middle East tensions and iron ore continued to edge higher.

Looking ahead, markets remain highly sensitive to global policy signals, geopolitical developments and the sustainability of the AI-driven rally, with volatility likely to remain elevated into year-end.

Defensive Income

The Prime Defensive portfolio produced a +0.27% return (before platform administration fees) over the month relative to a +0.30% target return. The portfolio has delivered a +6.36% return over the past 12 months, +2.25% above the target return.

October was a risk-off month in US fixed income, with spreads widening and yields falling, as the curve bull-flattened. Early in the month, softening employment data and government closures weighed on sentiment, while heightened US–China trade uncertainties later drove investors toward safe-haven assets, pushing 10y-and-2y yields to range lows of 3.94% and 3.42%, respectively. Later in the month, optimism surrounding a potential trade deal largely reversed the earlier risk-off trade and yields drifted higher, while the prior dovish expectations of the Fed rate path were tempered as inflation concerns heightened. The 10- and-2y yields closed the month -7bps and -4bps lower at 4.07% and 3.57%, respectively.

Domestically, credit performed, yields were broadly flat, and the curve bear flattened, as local inflation proves persistent. The ACGB 10y yield finished the month flat at 4.29%, and our ACGB 2y was +7bps higher at 3.55%, following a hotter-than-expected inflation print for 3Q25. This slight duration underperformance was offset by a tightening in local credit spreads. Our A$ B4 T2 FRN 5y index has now compressed below the 2021 tights to +125bps (clients can refer to our recent strategy note to see our thoughts on this market).

The top performer for the Portfolio PIMCO Global Bond Fund (+1.09%), contributing +10bps to performance as the off-shore risk-off trade drove capital returns.

During the month, we settled on our ~3.7% allocation to DMNHA, which traded softer than expected and detracted 3bps from portfolio performance. Although the underlying fundamentals remain robust, we expect technical factors that impacted trading conditions to continue challenging in the near term.

Australian Equities

The Prime Australian Equities Portfolio fell -0.41% in October.

Pilbara Minerals (+30.95%) was the standout contributor, rebounding strongly on improved lithium sentiment and stabilising spodumene prices. Codan (+22.80%) also delivered a solid gain, supported by robust demand for communications technology. ANZ Group (+10.36%) added positively as the banking sector benefited from stable credit conditions and resilient earnings. Rio Tinto (+8.88%) and BHP (+2.16%) contributed amid firm iron ore prices, while Nanosonics (+5.38%) rose on renewed optimism around its global distribution partnerships. Challenger (+7.51%).

On the other hand, several large-cap names weighed on performance. Wisetech Global (-23.41%) declined sharply following governance concerns and profit-taking after its strong prior run. CSL (-9.94%) detracted as margin pressures persisted in plasma and vaccines divisions, while Pro Medicus (-14.49%) fell on valuation concerns despite solid operational performance. Consumer names such as Wesfarmers (-9.42%) and Aristocrat Leisure (-9.47%) pulled back amid cautious discretionary spending trends. Coles (-9.74%) also weakened on margin pressure signals, while Santos (-6.24%) slipped despite firmer energy prices, reflecting project timing concerns.

Overall, October highlighted a clear divergence: resources and select financials provided strong support, while technology, healthcare, and consumer sectors dragged on returns. Stock selection remained critical, with concentrated gains in commodity-linked names helping offset notable weakness among several large-cap detractors.

International Equities

The Prime International Growth Portfolio returned 2.5% in October, navigating a month where equity markets remained resilient despite persistent inflation, rising bond yields and geopolitical uncertainty. Strength in US large caps linked to the ongoing AI cycle, alongside a strong rally in Japan and improving sentiment toward small- and mid-caps, helped drive gains, though performance across regions and styles remained uneven and continued to shape outcomes over both the month and the past year.

October performance was supported by strong contributions from Munro Global Growth Small & Mid Cap (4.7%), iShares Japan (4.6%), and Munro Concentrated Global Growth (4.6%), each benefiting from renewed interest in secular growth and the continued strength in Japanese corporates. However, this was offset by softer results from several key active managers. Langdon Global Smaller Companies (-1.6%), Trinetra Emerging Markets (-0.6%), and GQG Global Equity (-1.2%) were the largest detractors, with emerging markets and small-caps lagging the broader global index. Currency-hedged US exposure through the iShares S&P 500 AUD Hedged ETF (3.1%) also contributed modestly less amid a weaker Australian dollar.

Over the year, the portfolio returned 21.5%, driven primarily by strong selection within global growth. Munro Concentrated Global Growth (35.7%) and the iShares S&P 500 AUD Hedged ETF (19.0%) were standout contributors, supported by resilient US earnings and the dominance of mega-cap technology. However, GQG Global Equity (-5.5%), Langdon Global Smaller Companies (8.3%), and more limited exposure to unhedged global equities earlier in the year tempered results.

Overall, the portfolio participated meaningfully in global equity strength while maintaining balance across styles, with dispersion between growth leaders and more cyclically exposed strategies shaping performance over both periods.

Balanced Multi-asset

The Prime Balanced Portfolio returned 1.1% in October, demonstrating resilience during a month dominated by persistent inflation pressures, rising bond yields and uneven equity market leadership. Despite this backdrop, the portfolio’s diversification across income, growth and alternative strategies allowed it to participate across multiple drivers of return.

Fixed interest exposures provided a steady base, with PIMCO Global Bond (1.1%), MA Priority Income (0.6%) and Metrics Direct Income (0.7%) navigating the shift higher in yields while benefitting from still-firm credit markets. Real assets contributed positively, led by Clearbridge RARE Infrastructure (2.2%), which continued to benefit from stable cashflow characteristics. Alternatives again proved valuable, with Global X Physical Gold (6.1%) providing a notable uplift as investors continued to seek protection amid elevated geopolitical and macro uncertainty.

Within equities, domestic small caps delivered welcome strength through Spheria Australian Small Companies (3.8%). While internationally, strategies with small-cap or emerging-market tilts lagged, with Langdon Global Smaller Companies (-1.6%) and Trinetra Emerging Markets (-0.6%) detracting as investors favoured larger, more established global leaders. The iShares ASX 20 ETF (-1.0%) also moderated the equity contribution amid uneven local market performance.

Over the year to October, the portfolio returned 13.1%, supported by strong global growth exposures such as Munro Concentrated Global Growth (35.7%), resilient outcomes from income strategies and meaningful contributions from Betashares Ex-20 (16.4%). While some smaller-company and value-tilted strategies, including Langdon (8.3%) weighed at times, the portfolio’s balanced mix across regions, styles and asset classes enabled it to capture a wide range of return drivers over the year.

The information in this article contains general advice and is provided by Primestock Securities Ltd AFSL 239180. That advice has been prepared without taking your personal objectives, financial situation or needs into account. Before acting on this general advice, you should consider the appropriateness of it having regard to your personal objectives, financial situation and needs. You should obtain and read the Product Disclosure Statement (PDS) before making any decision to acquire any financial product referred to in this article. Please refer to the FSG (www.primefinancial.com.au/fsg) for contact information and information about remuneration and associations with product issuers. This information should not be relied upon as a substitute for professional advice, and we encourage you to seek specific advice from your professional adviser before making a decision on the matters discussed in this article. Information in this article is current at the date of this article, and we have no obligation to update or revise it as a result of any change in events, circumstances or conditions upon which it is based.