Market Data - July 2025

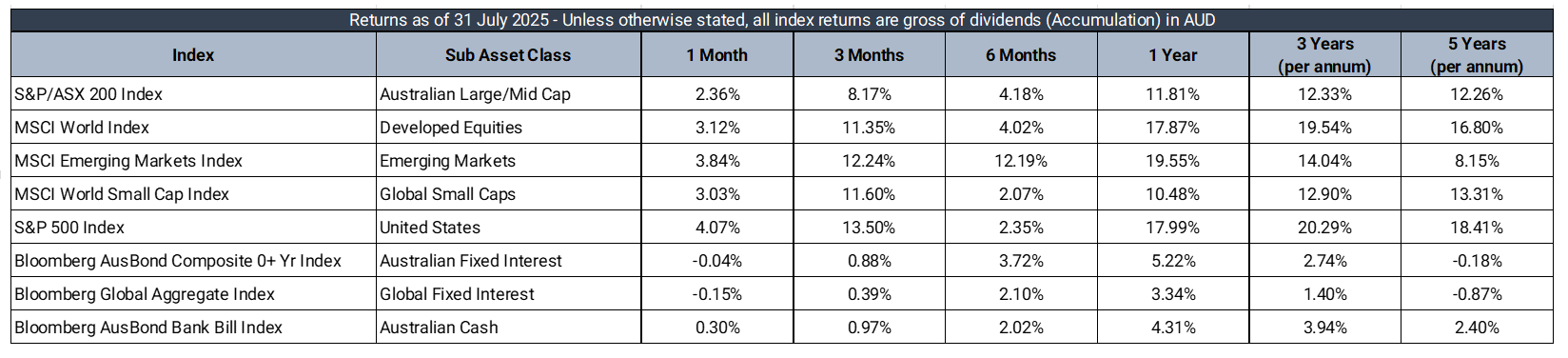

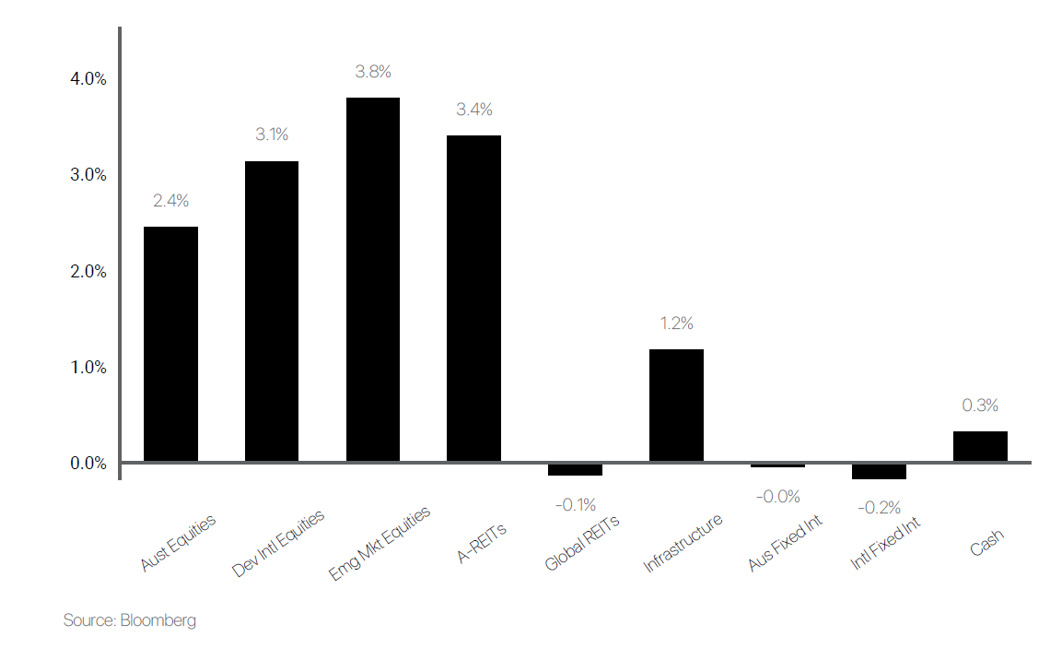

Market Returns - 1 Month to 31 July 2025 (in AUD)

Market Commentary

July 2025 saw global markets contend with a continued and complex mix of escalating trade frictions and divergent monetary policy signals. Early optimism—spurred by a resolution to the U.S.-Canada digital services tax dispute and signs of stabilisation in U.S.-China trade— quickly faded as Washington unveiled an array of surprise tariff announcements, signalling a more entrenched protectionist posture.

Global equities were broadly stable despite a more aggressive U.S. trade posture, which included 25-40% tariffs on key partners such as Japan, South Korea and South Africa. Sector performance was uneven, with cyclicals under pressure amid signs of margin compression as corporates absorbed tariff costs. European headline inflation held steady but industrial output softened, while Chinese and Japanese survey data surprised to the upside. Markets appeared either sceptical of full tariff implementation or confident in the limited economic impact in the near term.

Monetary policy dominated market narratives. U.S. rate-cut bets surged early in the month after Fed Chair Powell suggested rates would already be lower without tariff uncertainty but reversed following a firmer CPI print and robust Treasury auction demand. The Bank of England, by contrast, flagged multiple cuts from August.

In Australia, equities posted modest gains as the RBA kept rates unchanged, citing persistently high core inflation despite softer headline figures. Weak labour market data, including an unexpected rise in unemployment to 4.3% and a currency slide to US%0.65, strengthened expectations of potential earlier interest rate cuts.

Looking ahead, markets remain highly sensitive to trade developments as U.S. negotiations with key partners continue. Investors are closely watching economic data, corporate earnings guidance and central bank signals for guidance on grown and policy paths into Q3.

Defensive Income

The Prime Defensive portfolio produced a +0.49% return over the month relative to a +0.30% target return. The portfolio has delivered a +6.58% return over the past 12 months, a +2.27% above the target return.

Credit market performance varies in July as the reciprocal tariff "deadline" was once again deferred, this time to 1 August 2025. US economic data indicated disinflation had stalled, and Q2 growth was strong. Against this backdrop, the yield curve bear flattened, with the 2y yield rising +24bps to 3.96% and the 10y up +14bps to 4.37%. US Credit indices finished largely flat, as the CDX IG 5y tightened - 1bp to +51bps, and HY spread widened +5bps to +323bps, +5bps and +33bps from YTD tights respectively.

Domestically, spreads tightened and the yield curve mirrored the bear flattening seen in the US. The ACGB 10y yield increased by +10bps to 4.26%, and our 2y was up to +19bps to 3.40%. Initially, the RBA wrong-footed markets by holding rates, signalling it was awaiting Q2 inflation data to validate disinflation progress. Following the report, market expectations for a 25bps cut at the August meeting firmed, as trimmed mean CPI rose +2.7% YoY in Q2 (the lowest rate since Dec-2021). Local spreads tightened amid light supply, with our A$ True Corps BBB-rated 5y index tightening -12bps to +133bps, and our A$ B4 T2 FRN 5y index narrowing -22bps to +150bps.

The top performers for the Portfolio were Realm High Income Fund (+1.81%), and Yarra Higher Income Fund (+0.86%) contributing +9bps and +10bps respectively, supported by mark-to-market gains amid a domestic risk-on environment.

Following the settlement of LF1 at the end of June, our cash levels were on the lower side at ~2.3%. In July we have trimmed our allocation to Artesian, while also opportunistically reducing our exposure to LF1 selling down into a 1% premium to Nav. This has also repositioned the portfolio well to take advantage of any future spread spikes, or to support appropriate new products as they come to market.

Australian Equities

The Prime Australian Equities Portfolio gained 4.6% in July, significantly boosted by strength across several large-cap and growth-oriented holdings.

CSL (13.1%) was the top contributor, rebounding sharply on the back of robust earnings guidance and renewed investor confidence in its plasma division. Block (17.8%) also delivered strong gains as payment technology names rallied alongside global peers, benefiting from easing inflation pressures and signs of consumer resilience. Newmont (10.8%) was supported by higher gold prices, while Breville (11.5%) rose on positive trading updates and optimism around international sales growth.

Offsetting some of these gains were a handful of notable detractors. Macquarie Groups (-5.0%) eased as a weaker trading revenue guidance weighed on sentiment in the financial sector. Domino's Pizza (-5.2%) gave back some of its recent gains following cautious commentary on input cost pressures. Reece (-5.2%) and Treasury Wine Estates (-3.1%) also pulled back, the former on softer housing-related activity data and the latter amid mixed export market updates.

The month's results highlight the benefits of diversified sector and style allocation, with healthcare, technology, and materials leading gains. Stock selection played a key role, with several holdings delivering double-digit returns that more than offset weakness in select cyclical and consumer-focused names.

International Equities

The Prime International Growth Portfolio returned 2.2% in July, advancing in line with rising global markets but modestly trailing the strength seen in benchmark indices.

Positive contributions were led by the iShares S&P 500 AUD Hedged ETF (3.8%) and the Munro Concentrated Global Growth Fund (4.2%), both of which capitalised on the continued strength in U.S equities and the tech-led rally. Munro's high-conviction positioning in growth themes again proved effective, while hedged U.S. exposure benefited from broad-based gains and a softer Australian dollar. The Plato Global Alpha Fund (4.0%) also added value, extending its run of consistent monthly contributions.

Detractors included the GQG Partners Global Equity Fund (-1.1%), which lagged amid rotation back into high-growth stocks. Exposure to Japanese equities via the iShares MSCI Japan ETF (0.9%) also underwhelmed, as local market sentiment remained subdued despite attractive valuations. Cash holdings were a small drag in the context of a strongly rising market.

Over the year to July, the portfolio rose 17.6%, supported by strong active manager performance across core and thematic allocations. The Munro fund led with a return of 34.7%, while the iShares S&P 500 Hedged ETF delivered a strong 17.7%. Aoris International (16.5%) also contributed positively, reinforcing the strength of its quality first philosophy. The GQG fund remained the key laggard over the year (-2.9%), while modest underperformance from Japanese and value-tilted managers weighed slightly on relative performance.

The information in this article contains general advice and is provided by Primestock Securities Ltd AFSL 239180. That advice has been prepared without taking your personal objectives, financial situation or needs into account. Before acting on this general advice, you should consider the appropriateness of it having regard to your personal objectives, financial situation and needs. You should obtain and read the Product Disclosure Statement (PDS) before making any decision to acquire any financial product referred to in this article. Please refer to the FSG (www.primefinancial.com.au/fsg) for contact information and information about remuneration and associations with product issuers. This information should not be relied upon as a substitute for professional advice, and we encourage you to seek specific advice from your professional adviser before making a decision on the matters discussed in this article. Information in this article is current at the date of this article, and we have no obligation to update or revise it as a result of any change in events, circumstances or conditions upon which it is based.