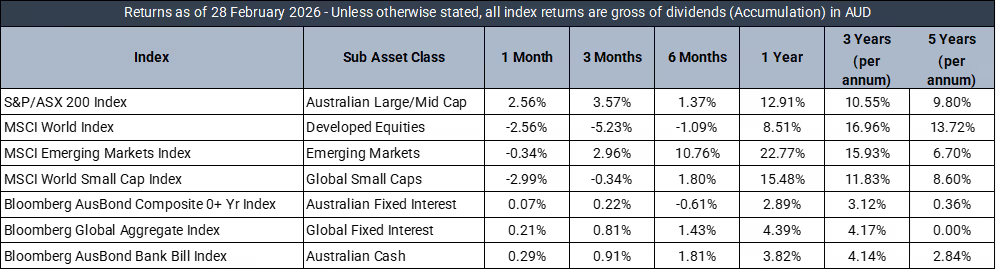

Market Data - February 2026

Market Returns - 1 Month to 28 February 2026 (in AUD)

Market Commentary

February 2026 ended with a major geopolitical shock, as US and Israeli airstrikes on Iran in the final days of the month triggered retaliatory missile strikes across the region. The escalation followed weeks of rising tensions and stalled nuclear negotiations, pushing oil prices higher and leaving equity markets cautious heading into March. This capped an already volatile month, as investors reassessed the AI trade amid increasing scrutiny of surging capital expenditure.

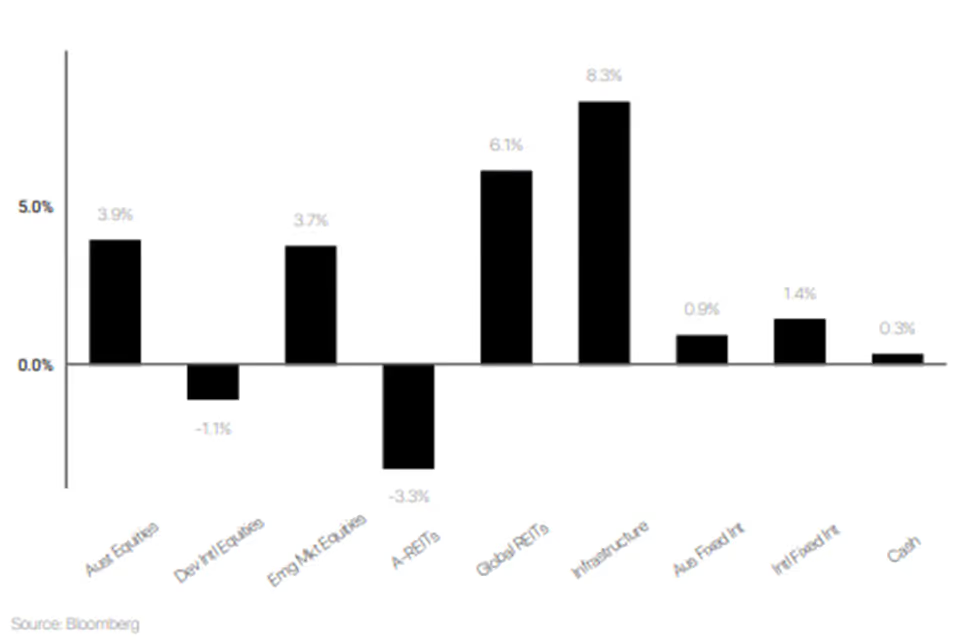

Global equity markets delivered mixed results. The S&P 500 declined 0.8% as investors rotated away from mega-cap technology, seeking clearer evidence of AI monetisation rather than continued capex expansion. In contrast, international developed markets rose 4.6%. Japanese equities rallied as manufacturing PMI reached a four year high of 52.8, while European equities also posted solid gains.

The Australian share market rose 4% in February, marking its strongest reporting season since 2017 as companies broadly exceeded earnings expectations despite rising geopolitical risks. Mining and financials led gains, with gold miners benefiting from elevated gold prices. Technology and healthcare lagged. Early in the month, the RBA raised the cash rate by 25 basis points to 3.85%, citing renewed inflation pressures and a still tight labour market.

In fixed income, higher domestic interest rates pushed Australian bond yields higher and weighed on prices. US yields also remained elevated as inflation concerns offset safe haven demand. Credit markets were more resilient, with corporate bonds holding up as company balance sheets remain broadly healthy.

Looking ahead, the conflict involving Iran has shifted the risk landscape entering March. Energy markets, shipping through the Strait of Hormuz, and global risk sentiment will likely dominate near term market movements as investors navigate what may be a volatile period.

Defensive Income

The Prime Defensive portfolio produced a +0.37% return (before platform administration fees) over the month relative to a +0.28% target return. The portfolio has delivered a +5.17% return over the past 12 months, +1.34% above the target return.

February was a largely risk-off month in credit markets as spreads broadly moved wider and yields fell. In the US, softer than anticipated inflation data, coupled with slowing growth indicators, led markets to price in more than two more rate cuts by the end of 2026. Risk sentiment stabilized pushing the term premium lower and causing a bull-flattening of the yield curve. The UST 2y yield fell 14bps to 3.38%, while the 10y fell 30bps to 3.94%. However, credit spreads widened amid concerns about private credit, slowing growth and excessive corporate capital expenditure guidance following earnings. The 5y IG CDX widened 7bps to +56bps and HY CDX widened 36bps to +332bps.

In Australia, the yield curve bull flattened as expectations for near term rates remained largely stable, while the term premium fell on a risk-off move. As a result, domestic duration outperformed, reversing the trend of the three months prior, with the ACGB 10y yield falling -16bps to 4.65% and the 2y easing -2bps to 4.19%. The risk-off move saw domestic spreads move wider, with A$ Big Four Tier 2 5-year FRN index widening 20bps to +133bps and A$ Big Four Senior Unsecured index widening 5bps to +71bps.

Portfolio performance was largely positive over the month, with strong contributions from Pimco Global Bond Fund (+1.29%) and Pendal Government Bond Fund (+0.97%), as both offshore and domestic duration outperformed. CIMHA dragged on returns, as trading performance in the listed note market remains volatile on low volumes, yet we remain comfortable with the underlying fundamentals.

Last month we introduced the Barings Liquidity Investment Strategy, allocating ~4% of the portfolio. In our first full month of holding, it delivered a stable +0.38% HPR. Given its exposure to RMBS loans, we expect this allocation to provide consistent returns with minimal sensitivity to broader market movements.

Australian Equities

The Australian Growth portfolio returned 2.57% in February 2026, underperforming the 4.11% rise in the S&P/ASX 200 Accumulation Index. The Australian Growth portfolio weakened in February 2026 as ASX markets rotated away from higher valuation growth and defensive stocks toward cyclicals and resources. Sentiment was pressured by persistent inflation, rising bond yields, and reduced confidence in near‑term rate cuts, which drove valuation compression across interest rate‑sensitive sectors such as healthcare, technology, and property.

Portfolio performance was most impacted by declines in healthcare and growth names, including Pro Medicus (‑29.15%), Cochlear (‑26.05%), CSL (‑19.10%) and Aristocrat (‑10.23%), alongside weakness in consumer and REIT exposures such as REA (‑12.31%) and Goodman Group (‑5.82%). These falls were partially offset by strength across cyclicals and resources, led by Pilbara Minerals (+20.98%), BHP (+15.50%), NAB (+13.03%), Evolution Mining (+12.71%) and Rio Tinto (+10.41%), supported by firmer commodity prices and more resilient earnings from miners and banks.

International Equities

The Prime International Growth Portfolio returned 0.5% in February 2026, holding up well in a month where global equity markets delivered mixed results amid escalating geopolitical tensions in the Middle East and growing scrutiny of AI related capital expenditure. Japanese equities were a standout, with the iShares MSCI Japan ETF (+6.4%) rallying as manufacturing activity reached multi year highs. The Munro Global Growth Small and Mid Cap Fund (+7.0%) was the portfolio's strongest performer, benefiting from similar tailwinds in international markets. European equities also contributed through the iShares Europe ETF (+1.6%), while the Pzena Global Focused Value Fund (+1.8%) added to returns as value oriented strategies found support. On the other side, the Langdon Global Smaller Companies Fund (-5.0%) was the largest detractor as smaller companies bore the brunt of risk aversion late in the month. The Macquarie IFP Global Franchise Fund (-2.9%) and the Aoris International Fund (-2.3%) also weighed on performance.

Over the twelve months to February 2026, the portfolio's core allocation to the iShares S&P 500 Hedged ETF (+27.6%) and iShares MSCI Japan ETF (+24.2%) have been the primary drivers of returns, supported by contributions from the Plato Global Alpha Fund (+15.8%) and the iShares Europe ETF (+15.5%). However, this has been partially offset by headwinds from the Langdon Global Smaller Companies Fund (-7.5%) and the Aoris International Fund (-9.3%), both of which have struggled in a market environment that has broadly favoured larger capitalisation growth names. The exit from the GQG Partners Global Equity Fund (-12.5%) also weighed on the twelve month result.

Balanced Multi-asset

The Prime Balanced Portfolio returned 1.0% in February 2026, a month shaped by mixed reporting season outcomes domestically, divergent global equity performance, and escalating geopolitical tensions following US and Israeli airstrikes on Iran late in the month.

Property and infrastructure holdings were the standout contributors, as the Resolute Capital Global Property Securities Fund (+7.7%), CBI RARE Infrastructure Fund (+7.1%), and Vanguard Global Infrastructure ETF (+6.4%) all rallied strongly alongside global listed real assets. International equities were similarly positive, with the iShares MSCI Japan ETF (+6.4%) and Munro Global Growth Small and Mid Cap Fund (+7.0%) delivering strong returns. However, Australian small cap exposures weighed heavily on the month, with the Ophir High Conviction Fund (-11.1%) and Langdon Global Smaller Companies Fund (-5.0%) detracting as smaller companies lagged the broader market during reporting season. The BetaShares Australian Ex-20 Portfolio (-1.5%) also underperformed as gains were concentrated in the largest names on the ASX.

Over the twelve months to the end of February, the portfolio has benefited from diversification across regions and asset classes. The allocation to physical gold (+57.9%) was the most significant contributor as geopolitical uncertainty and central bank buying drove prices to record levels. Global equities added meaningfully, led by the iShares S&P 500 AUD Hedged ETF (+27.6%), the iShares MSCI Japan ETF (+24.2%), and the Vanguard FTSE All World ex US ETF (+22.8%). Infrastructure also contributed through CBI RARE (+19.6%). Offsetting these gains, the Ophir High Conviction Fund (-10.6%) and the Langdon Global Smaller Companies Fund (-7.5%) detracted over the year as global smaller companies faced persistent headwinds from elevated interest rates and cautious investor sentiment toward less liquid parts of the market.

The information in this article contains general advice and is provided by Primestock Securities Ltd AFSL 239180. That advice has been prepared without taking your personal objectives, financial situation or needs into account. Before acting on this general advice, you should consider the appropriateness of it having regard to your personal objectives, financial situation and needs. You should obtain and read the Product Disclosure Statement (PDS) before making any decision to acquire any financial product referred to in this article. Please refer to the FSG (www.primefinancial.com.au/fsg) for contact information and information about remuneration and associations with product issuers. This information should not be relied upon as a substitute for professional advice, and we encourage you to seek specific advice from your professional adviser before making a decision on the matters discussed in this article. Information in this article is current at the date of this article, and we have no obligation to update or revise it as a result of any change in events, circumstances or conditions upon which it is based.